Indicators Module¶

BinPan own indicators and utils.

Functions:

|

Obtains the minim value for fractal_w periods as fractal is pure alternating max to mins. In other words, max and mins alternates |

|

Obtains the trend of the fractal_w indicator. |

|

Applies the fractal_trend_indicator function to the dataframe df for each index flagged with 1 in the flags series. |

|

The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. |

|

Kaufman's Efficiency Ratio based in: https://stackoverflow.com/questions/36980238/calculating-kaufmans-efficiency-ratio-in-python -with-pandas |

|

The fractal indicator is based on a simple price pattern that is frequently seen in financial markets. |

|

Calculates support and resistance levels based on volume and prices in the given dataframe. |

Calcula el número de valores que cada entrada en la serie supera hacia atrás hasta encontrar un valor superior o llegar al inicio de la serie. |

|

Calcula el número de valores que son superiores a cada entrada en la serie hacia atrás hasta encontrar un valor igual o menor o llegar al inicio de la serie. |

|

|

Calculate the rolling maximum and the steps back to the maximum for each point in the series. |

|

Calculate the rolling minimum and the steps back to the minimum for each point in the series. |

|

Splits a serie by values of other serie in four series by relative positions for plotting colored clouds with plotly. |

|

Splits a dataframe y sub dataframes to plot by colored areas. |

It zooms the cloud indicators in an index interval for a plot zoom. |

|

|

It shifts a candle ahead by the window argument value (or backwards if negative). |

|

It forward fills a value through nans while a window of candles ahead. |

|

Generate reversal candles for reversal charts: |

|

Optimized version of repeating prices by quantity for K-means clustering, with a comparison between 'Quantity' and 'Quote quantity' to choose the column with larger values for repeating prices. |

|

Generate initial centroids for K-means clustering with equally spaced values between min and max values in data. |

|

Find the optimal quantity of centroids for support and resistance methods using the elbow method. |

|

Calculate support and resistance levels for a given set of trades using K-means clustering. |

|

Calculate support and resistance levels merged for a given set of trades using K-means clustering. |

|

Repeat timestamps by quantity to give more importance to prices with more quantity. |

|

Calculate support and resistance levels timestamp centroids for a given set of trades using K-means clustering. |

Calculate the market profile for a given OHLC data. |

|

Calculate the ratio of taker and maker volume for a given OHLC data. |

|

|

Calculate the market profile for a given OHLC data. |

|

Calculate the market profile for a given trades data. |

|

Calcula POC, Value Area y nodos de alto/bajo volumen de un market profile. |

|

Average True Range using Wilder's smoothing (RMA). |

|

Supertrend indicator (Binance-compatible). |

|

Moving Average Convergence/Divergence. |

|

Stochastic RSI. |

|

On Balance Volume. |

|

Accumulation/Distribution line. |

|

Volume Weighted Average Price (cumulative over the full series). |

|

Commodity Channel Index. |

|

Ease of Movement. |

|

Rate of Change. |

|

Bollinger Bands. |

|

Stochastic Oscillator. |

- alternating_fractal_indicator(df: DataFrame, max_period: int = None, suffix: str = '') DataFrame | None[source]¶

- Obtains the minim value for fractal_w periods as fractal is pure alternating max to mins. In other words, max and mins alternates

in regular rhythm without any tow max or two mins consecutively.

- This custom indicator shows the minimum period in finding a pure alternating fractal. It is some kind of volatility in price

indicator, the most period needed, the most volatile price.

- Parameters:

- Return pd.DataFrame:

A dataframe with two columns, one with 1 or -1 for local max or local min to tag, and other with price values for that points. If not found, it will return None.

- fractal_trend_indicator(df: DataFrame, period: int = None, fractal: DataFrame = None, suffix: str = '') tuple | None[source]¶

Obtains the trend of the fractal_w indicator. It will return maximums diff mean and minimums diff mean also in a tuple.

- Parameters:

- Return tuple:

Max min diffs mean and Min diffs mean.

- calculate_fractal_trend_on_flags(df: DataFrame, flags: Series, period: int = None, suffix: str = '') list[tuple][source]¶

Applies the fractal_trend_indicator function to the dataframe df for each index flagged with 1 in the flags series.

This function is designed to work with a DatetimeIndex.

- Parameters:

- Returns:

A list of tuples with the results of fractal_trend_indicator for each flagged index.

- ichimoku(data: DataFrame, tenkan: int = 9, kijun: int = 26, chikou_span: int = 26, senkou_cloud_base: int = 52, suffix: str = '') DataFrame[source]¶

The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. It does this by taking multiple averages and plotting them on a chart. It also uses these figures to compute a “cloud” that attempts to forecast where the price may find support or resistance in the future.

https://school.stockcharts.com/doku.php?id=technical_indicators:ichimoku_cloud

https://www.youtube.com/watch?v=mCri-FFvZjo&list=PLv-cA-4O3y97HAd9OCvVKSfvQ8kkAGKlf&index=7

- Parameters:

data (pd.DataFrame) – A BinPan Symbol dataframe.

tenkan (int) – The short period. It’s the half sum of max and min price in the window. Default: 9

kijun (int) – The long period. It’s the half sum of max and min price in the window. Default: 26

chikou_span (int) – Close of the next 26 bars. Util when spotting what happened with other ichimoku lines and what happened before Default: 26.

senkou_cloud_base – Period to obtain kumo cloud base line. Default is 52.

suffix (str) – A decorative suffix for the name of the column created.

- Return pd.DataFrame:

A pandas dataframe with columns as indicator lines.

import binpan sym = binpan.Symbol(symbol='LUNCBUSD', tick_interval='1m', limit=500) sym.ichimoku() sym.plot()

- ker(close: Series, window: int) Series[source]¶

Kaufman’s Efficiency Ratio based in: https://stackoverflow.com/questions/36980238/calculating-kaufmans-efficiency-ratio-in-python -with-pandas

- Parameters:

close (pd.Series) – Close prices serie.

window (int) – Window to check indicator.

- Return pd.Series:

Results.

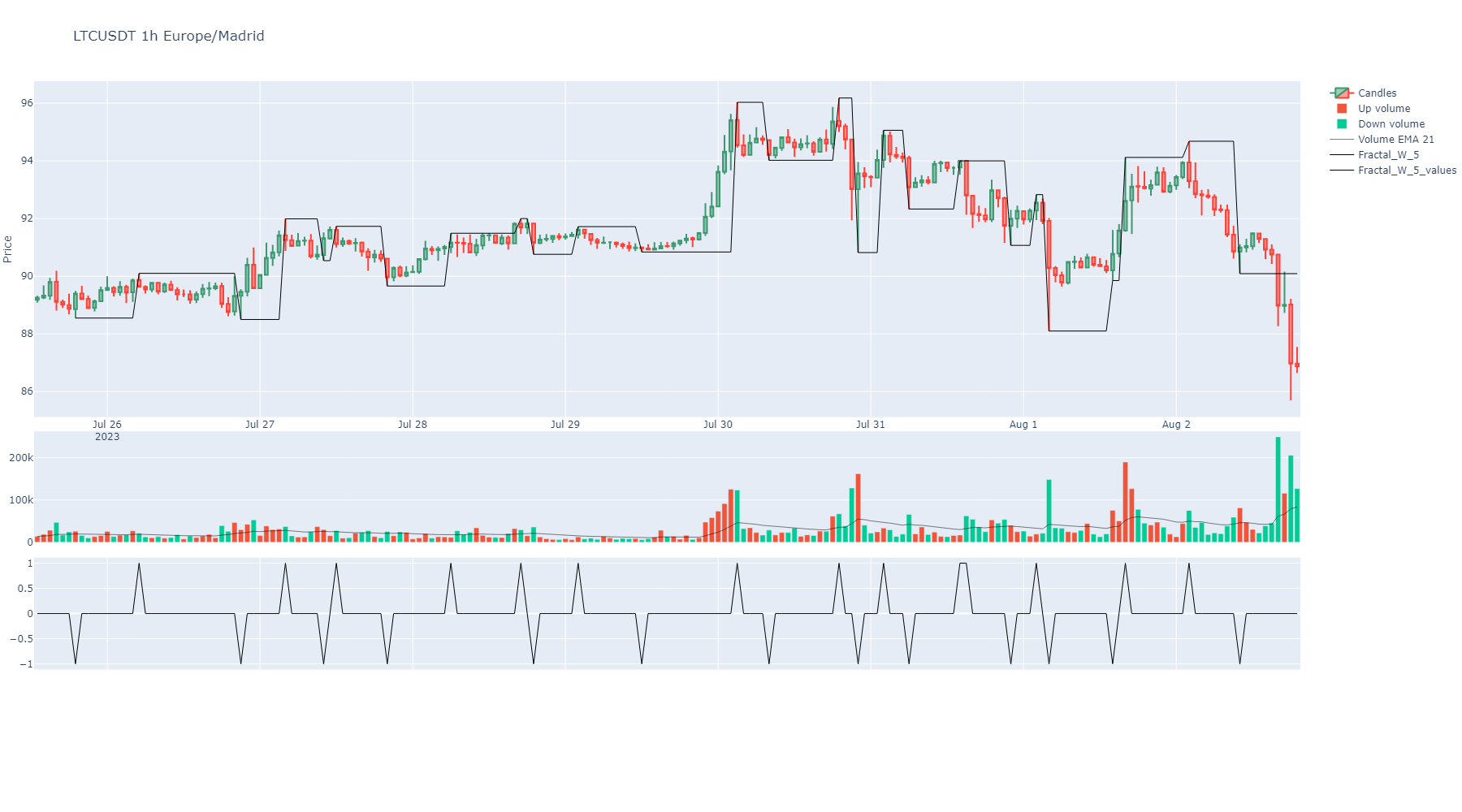

- fractal_w_indicator(df: DataFrame, period=2, merged: bool = True, suffix: str = '', fill_with_zero: bool = None) DataFrame[source]¶

The fractal indicator is based on a simple price pattern that is frequently seen in financial markets. Outside of trading, a fractal is a recurring geometric pattern that is repeated on all time frames. From this concept, the fractal indicator was devised. The indicator isolates potential turning points on a price chart. It then draws arrows to indicate the existence of a pattern.

- Parameters:

df (pd.DataFrame) – BinPan dataframe with High prices.

period (int) – Default is 2. Count of neighbour candles to match max or min tags.

merged (bool) – If True, values are merged into one pd.Serie. minimums overwrite maximums in case of coincidence.

suffix (str) – A decorative suffix for the name of the column created.

fill_with_zero (bool) – If true fills nans with zeros. Its better to plot with binpan.

- Return pd.DataFrame:

A dataframe with two columns, one with 1 or -1 for local max or local min to tag, and other with price values for that points.

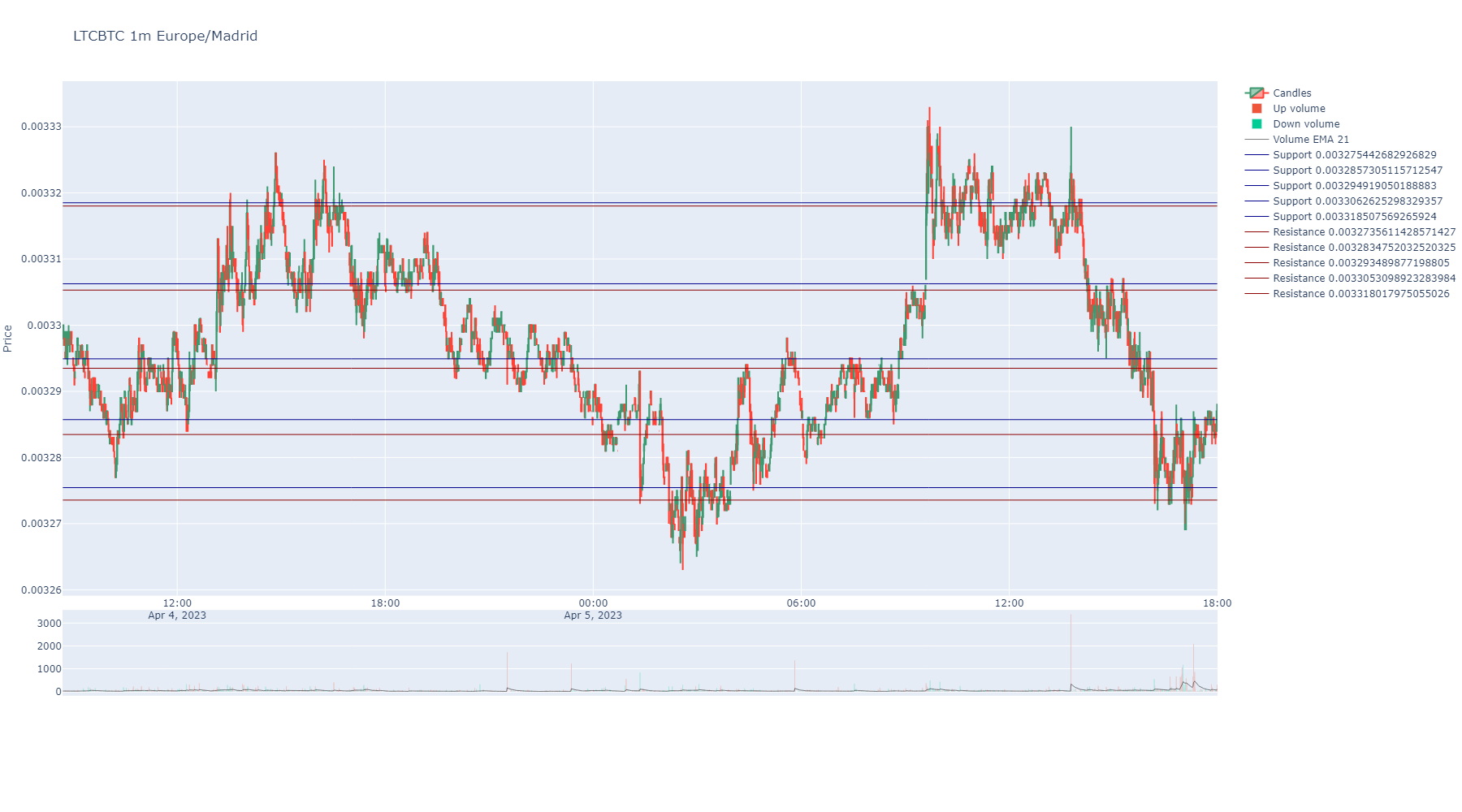

- support_resistance_volume(df, num_bins=100, price_col='Close', volume_col='Volume', threshold=90) list[source]¶

Calculates support and resistance levels based on volume and prices in the given dataframe.

- Parameters:

df (pd.DataFrame) – The dataframe containing price and volume data.

num_bins (int) – Optional. The number of bins to use for accumulating volume. Default is 100.

price_col (str) – Optional. The name of the column containing price data. Default is ‘Close’.

volume_col (str) – Optional. The name of the column containing volume data. Default is ‘Volume’.

threshold (int) – Percentil to show most traded levels. Default is 90. The threshold variable filters the volume levels considered when calculating support and resistance levels. A higher threshold results in fewer levels, based on higher transaction volumes, while a lower threshold yields more levels, based on a broader range of transaction volumes.

- Return list:

A sorted list of support and resistance levels.

- count_smaller_values_backward(s: Series | list) Series[source]¶

Calcula el número de valores que cada entrada en la serie supera hacia atrás hasta encontrar un valor superior o llegar al inicio de la serie.

- Parameters:

s – Serie de pandas o lista de números.

- Returns:

Serie de pandas con el número de valores que cada entrada supera hacia atrás.

- count_larger_values_backward(s: Series | list) Series[source]¶

Calcula el número de valores que son superiores a cada entrada en la serie hacia atrás hasta encontrar un valor igual o menor o llegar al inicio de la serie.

- Parameters:

s – Serie de pandas o lista de números.

- Returns:

Serie de pandas con el número de valores que son superiores a cada entrada hacia atrás.

- rolling_max_with_steps_back(ser: Series, window: int, pct_diff: bool = True) -> (<class 'pandas.core.series.Series'>, <class 'pandas.core.series.Series'>)[source]¶

Calculate the rolling maximum and the steps back to the maximum for each point in the series.

Parameters: series (pd.Series): The time series of prices. window (int): The rolling window size. pct_result (bool): If True, the maximum values are returned as percentages instead of absolute values (default True).

Returns: pd.Series: A series of the rolling maximum values. pd.Series: A series indicating the number of steps back to the maximum value within the window.

- rolling_min_with_steps_back(ser: Series, window: int, pct_diff: bool = True) -> (<class 'pandas.core.series.Series'>, <class 'pandas.core.series.Series'>)[source]¶

Calculate the rolling minimum and the steps back to the minimum for each point in the series.

Parameters: series (pd.Series): The time series of prices. window (int): The rolling window size. pct_result (bool): If True, the minimum values are returned as percentages instead of absolute values (default True).

Returns: pd.Series: A series of the rolling minimum values. pd.Series: A series indicating the number of steps back to the minimum value within the window.

- split_serie_by_position(serie: Series, splitter_serie: Series, fill_with_zeros: bool = True) DataFrame[source]¶

Splits a serie by values of other serie in four series by relative positions for plotting colored clouds with plotly.

This means you will get 4 series with different situations:

serie is over the splitter serie.

serie is below the splitter serie.

splitter serie is over the serie.

splitter serie is below the serie.

- Parameters:

serie (pd.Series) – A serie to classify in reference to other serie.

splitter_serie (pd.Series) – A serie to split in two couple of series classified by position reference.

fill_with_zeros (bool) – Fill nans with zeros for splitted lines like MACD to avoid artifacts in plots.

- Return tuple:

A tuple with four series classified by upper position or lower position.

- df_splitter(data: DataFrame, up_column: str, down_column: str) list[source]¶

Splits a dataframe y sub dataframes to plot by colored areas.

- zoom_cloud_indicators(plot_splitted_serie_couples: dict, main_index: list, start_idx: int, end_idx: int) dict[source]¶

It zooms the cloud indicators in an index interval for a plot zoom.

- shift_indicator(serie: Series, window: int = 1) Series[source]¶

It shifts a candle ahead by the window argument value (or backwards if negative).

Just works with time indexes.

- Parameters:

serie (pd.Series) – A pandas Series.

window (int) – Times values are shifted ahead. Default is 1.

- Return pd.Series:

A series with index adjusted to the new shifted positions of values.

- ffill_indicator(serie: Series, window: int = 1) Series[source]¶

It forward fills a value through nans while a window of candles ahead.

- Parameters:

serie (pd.Series) – A pandas Series.

window (int) – Times values are shifted ahead. Default is 1.

- Return pd.Series:

A series with index adjusted to the new shifted positions of values.

- reversal_candles(trades: DataFrame, decimal_positions: int, time_zone: str, min_height: int = 7, min_reversal: int = 4) DataFrame[source]¶

- Generate reversal candles for reversal charts:

- Parameters:

trades (pd.Series) – A dataframe with trades sizes, side and prices.

decimal_positions (int) – Because this function uses integer numbers for prices, is needed to convert prices. Just steps are relevant.

time_zone (str) – A time zone like “Europe/Madrid”.

min_height (int) – Minimum candles height in pips.

min_reversal (int) – Maximum reversal to close the candles

- Return pd.DataFrame:

A serie with the resulting candles number sequence.

- Example:

import binpan ltc = binpan.Symbol(symbol='ltcbtc', tick_interval='5m', time_zone = 'Europe/Madrid', time_index = True, closed = True, hours=5) ltc.get_trades() ltc.get_reversal_candles() ltc.plot_reversal()

- repeat_prices_by_quantity(data: DataFrame, price_col='Price', qty_col='Quantity', alt_qty_col='Quote quantity') ndarray[source]¶

Optimized version of repeating prices by quantity for K-means clustering, with a comparison between ‘Quantity’ and ‘Quote quantity’ to choose the column with larger values for repeating prices.

- Parameters:

data (pd.DataFrame) – A pandas DataFrame with trades or klines, containing ‘Price’, ‘Quantity’, and optionally ‘Quote quantity’ columns.

price_col (str) – The name of the column containing price data. Default is ‘Price’.

qty_col (str) – The primary name of the column containing quantity data. Default is ‘Quantity’.

alt_qty_col (str) – The alternative name of the column containing quantity data to compare with qty_col. Default is ‘Quote quantity’.

- Return np.ndarray:

A numpy array with the prices repeated by the chosen quantity.

- kmeans_custom_init(data: ndarray, max_clusters: int) ndarray[source]¶

Generate initial centroids for K-means clustering with equally spaced values between min and max values in data. :param data: A data array. :param max_clusters: Max clusters expected. :return: A numpy array with initial centroids.

- find_optimal_clusters(KMeans_lib, data: ndarray, max_clusters: int, quiet: bool = False, initial_centroids: list | ndarray = None, sample_weight: ndarray = None) int[source]¶

Find the optimal quantity of centroids for support and resistance methods using the elbow method.

- Parameters:

KMeans_lib – A KMeans library to use.

data – A numpy array with the data to analyze.

max_clusters – Maximum number of clusters to consider.

quiet (bool) – If true, do not print progress bar.

initial_centroids (list) – Initial centroids to use optionally for faster results.

sample_weight (np.ndarray) – Optional sample weights for weighted KMeans.

- Returns:

The optimal number of clusters (centroids) as an integer.

- support_resistance_levels(df: DataFrame, max_clusters: int = 5, by_quantity: bool = None, by_klines=True, optimize_clusters_qty: bool = False) tuple[source]¶

Calculate support and resistance levels for a given set of trades using K-means clustering.

- Parameters:

df – A pandas DataFrame with trades or klines, containing a ‘Price’, ‘Quantity’ columns and a ‘Buyer was maker’ column, if trades passed, else “Close”, “Volume” and “Taker buy base volume”

max_clusters – Maximum number of clusters to consider for finding the optimal number of centroids. Default: 5.

by_quantity (float) – Count each price as many times the quantity contains a float of a the passed amount. Example: If a price 0.001 has a quantity of 100 and by_quantity is 0.1, quantity/by_quantity = 100/0.1 = 1000, then this prices is taken into account 1000 times instead of 1.

by_klines (bool) – If true, data is assumed to be klines.

optimize_clusters_qty (bool) – If true, find the optimal number of clusters to use for calculating support and resistance levels.

- Returns:

A tuple containing two lists: the first list contains the support levels, and the second list contains the resistance levels. Both lists contain float values.

- support_resistance_levels_merged(df: DataFrame, by_klines: bool, max_clusters: int = 5, by_quantity: float = True, optimize_clusters_qty: bool = False)[source]¶

Calculate support and resistance levels merged for a given set of trades using K-means clustering.

Uses

sample_weightin KMeans instead of repeating prices, avoiding MemoryError with large volumes.- Parameters:

df – A pandas DataFrame with trades or klines, containing a ‘Price’, ‘Quantity’ columns or “Close”, “Volume”.

by_klines – If true, assume data is from klines.

max_clusters – Quantity of clusters to consider initially. Default: 5.

by_quantity – If true, use quantity to weight prices. It gives more importance to prices with more quantity.

optimize_clusters_qty – If true, find the optimal number of clusters to use for calculating support and resistance levels.

- Returns:

A list containing the support and resistance levels merged. It would be just levels.

- repeat_timestamps_by_quantity(df: DataFrame, epsilon_quantity: float, buy_maker: bool = None, buy_taker: bool = None, trades_col_from_kline: str = 'Trades') ndarray[source]¶

Repeat timestamps by quantity to give more importance to prices with more quantity. It detects if data is from trades or klines by column names.

- Parameters:

df – A pandas DataFrame with trades or klines, containing a ‘Price’, ‘Quantity’ columns or “Close”, “Volume” respectively.

epsilon_quantity – Quantity to repeat timestamps by.

buy_maker – If true, use maker side volume.

buy_taker – If true, use taker side volume.

trades_col_from_kline – If true, use taker side volume.

- Returns:

- time_active_zones(df: DataFrame, max_clusters: int = 5, simple: bool = True, by_quantity: float = True, quiet=False, optimize_clusters_qty: bool = False) tuple[source]¶

Calculate support and resistance levels timestamp centroids for a given set of trades using K-means clustering.

- Parameters:

df – A pandas DataFrame with trades or klines, containing a ‘Price’, ‘Quantity’ columns and a ‘Buyer was maker’ column, if trades passed, else “Close”, “Volume” and “Taker buy base volume”

max_clusters – Maximum number of clusters to consider for finding the optimal number of centroids. Default: 5.

simple (bool) – If true, use all trades to calculate time activity clusters.

by_quantity (float) – Count each price as many times the quantity contains a float of a the passed amount. Example: If a price 0.001 has a quantity of 100 and by_quantity is 0.1, quantity/by_quantity = 100/0.1 = 1000, then this prices is taken into account 1000 times instead of 1.

quiet (bool) – If true, do not print progress bar.

optimize_clusters_qty (bool) – If true, find the optimal number of clusters to use for calculating support and resistance levels.

- Returns:

A tuple containing two lists: the first list contains the support levels, and the second list contains the resistance levels. Both lists contain float values.

- market_profile_from_klines_melt(df: DataFrame) DataFrame[source]¶

Calculate the market profile for a given OHLC data. The function calculates the average price for each candle (high + low + close) / 3, and then calculates the ‘maker’ and ‘taker’ volumes for each average price.

- Parameters:

df – A pandas DataFrame with the OHLC data. It should contain ‘High’, ‘Low’, ‘Close’, ‘Volume’, and ‘Taker buy base volume’ columns.

- Returns:

A pandas DataFrame grouped by the average price (‘Market_Profile’) with the sum of ‘Taker buy base volume’ and ‘Maker_Volume’ for each average price.

- taker_maker_profile_from_klines_melt(df: DataFrame) DataFrame[source]¶

Calculate the ratio of taker and maker volume for a given OHLC data.

- Parameters:

df – A pandas DataFrame with the OHLC data. It should contain ‘High’, ‘Low’, ‘Close’, ‘Volume’, and ‘Taker buy base volume’ columns.

- Returns:

A pandas DataFrame grouped by the average price (‘Market_Profile’) with the sum of ‘Taker buy base volume’ and ‘Maker_Volume’ for each average price.

- market_profile_from_klines_grouped(df: DataFrame, num_bins: int = 100) DataFrame[source]¶

Calculate the market profile for a given OHLC data. The function calculates the average price for each candle (high + low + close) / 3, and then calculates the ‘maker’ and ‘taker’ volumes for each average price.

- Parameters:

df – A pandas DataFrame with the OHLC data. It should contain ‘High’, ‘Low’, ‘Close’, ‘Volume’, and ‘Taker buy base volume’ columns.

num_bins (int) – Number of bins to use for the market profile.

- Returns:

A pandas DataFrame grouped by the average price (‘Market_Profile’) with the sum of ‘Taker buy base volume’ and ‘Maker_Volume’ for each average price.

- market_profile_from_trades_grouped(df: DataFrame, num_bins: int = 100) DataFrame[source]¶

Calculate the market profile for a given trades data. The function calculates the average price for each trade and then calculates the ‘maker’ and ‘taker’ volumes for each average price.

- Parameters:

df – A pandas DataFrame with the trades data. It should contain ‘Price’, ‘Quantity’, ‘Buyer was maker’ columns.

num_bins – The number of bins to use for the market profile.

- Returns:

A pandas DataFrame grouped by the average price (‘Price_Bin’) with the sum of ‘Taker buy base volume’ and ‘Maker buy base volume’ for each average price.

- value_area_from_profile(profile: DataFrame, value_area_pct: float = 0.7) dict | None[source]¶

Calcula POC, Value Area y nodos de alto/bajo volumen de un market profile.

A partir de un DataFrame de market profile (el que devuelven

market_profile_from_klines_groupedomarket_profile_from_trades_grouped:IntervalIndexde precio + columnas de volumen) calcula las metricas tipicas de un Volume Profile (VPVR):POC (Point of Control): el nivel de precio con mayor volumen, el gran iman.

Value Area (VAH/VAL): el rango de precios que concentra

value_area_pctdel volumen total, expandido desde el POC hacia el vecino con mas volumen en cada paso (algoritmo estandar).HVN / LVN (High/Low Volume Nodes): maximos/minimos locales del histograma. Los HVN actuan como soportes/resistencias por aceptacion; los LVN son huecos por donde el precio viaja rapido.

- Parameters:

profile (pd.DataFrame) – market profile con

IntervalIndexde precio. El volumen de cada bin es la suma de todas sus columnas numericas (taker + maker).value_area_pct (float) – fraccion del volumen total dentro de la Value Area. Por defecto 0.70.

- Returns:

dict con

poc,vah,val,value_area_pct,total_volume,bins(lista de{price, low, high, volume}),hvnylvn(listas de precios).Nonesi el perfil esta vacio.

Ejemplo:

prof = market_profile_from_klines_grouped(df=sym.df, num_bins=50) va = value_area_from_profile(prof, value_area_pct=0.70) print(va["poc"], va["vah"], va["val"])

- atr(high: Series, low: Series, close: Series, length: int = 14) Series[source]¶

Average True Range using Wilder’s smoothing (RMA).

- Parameters:

high (pd.Series) – High prices.

low (pd.Series) – Low prices.

close (pd.Series) – Close prices.

length (int) – Period. Default 14.

- Return pd.Series:

ATR values with column name

ATRr_{length}.

- supertrend(high: Series, low: Series, close: Series, length: int = 10, multiplier: float = 3.0) DataFrame[source]¶

Supertrend indicator (Binance-compatible).

- macd(close: Series, fast: int = 12, slow: int = 26, signal: int = 9) DataFrame[source]¶

Moving Average Convergence/Divergence.

- stoch_rsi(close: Series, rsi_length: int = 14, stoch_length: int = 14, k_smooth: int = 3, d_smooth: int = 3) DataFrame[source]¶

Stochastic RSI.

- obv(close: Series, volume: Series) Series[source]¶

On Balance Volume.

- Parameters:

close (pd.Series) – Close prices.

volume (pd.Series) – Volume.

- Return pd.Series:

OBV values.

- ad(high: Series, low: Series, close: Series, volume: Series) Series[source]¶

Accumulation/Distribution line.

- Parameters:

high (pd.Series) – High prices.

low (pd.Series) – Low prices.

close (pd.Series) – Close prices.

volume (pd.Series) – Volume.

- Return pd.Series:

AD values.

- vwap(high: Series, low: Series, close: Series, volume: Series) Series[source]¶

Volume Weighted Average Price (cumulative over the full series).

- Parameters:

high (pd.Series) – High prices.

low (pd.Series) – Low prices.

close (pd.Series) – Close prices.

volume (pd.Series) – Volume.

- Return pd.Series:

VWAP values.

- cci(high: Series, low: Series, close: Series, length: int = 14, c: float = 0.015) Series[source]¶

Commodity Channel Index.

- eom(high: Series, low: Series, volume: Series, length: int = 14, divisor: int = 100000000) Series[source]¶

Ease of Movement.

- bbands(close: Series, length: int = 5, std: float = 2.0, ddof: int = 0) DataFrame[source]¶

Bollinger Bands.