BinPan Module¶

import binpan

Symbol Class¶

The main entry point in BinPan. Fetches candlestick (kline) data from the Binance API and provides methods for technical indicators, plotting, trade analysis, and strategy backtesting.

The Symbol class uses a mixin architecture:

SymbolIndicators: technical indicators (EMA, RSI, MACD, Bollinger Bands, etc.)

SymbolPlotting: candlestick charts, trade visualizations, order book plots

SymbolStrategy: tagging, cross detection, backtesting engine

Example notebooks are in the notebooks/ folder of the repository.

- class Symbol(symbol: str = None, tick_interval: str = None, start_time: int | str = None, end_time: int | str = None, limit: int = 1000, time_zone: str = 'Europe/Madrid', closed: bool = True, hours: float = None, postgres_klines: bool | str = False, postgres_agg_trades: bool | str = False, postgres_atomic_trades: bool | str = False, binbase: bool | str = False, display_columns: int = 25, display_max_rows: int = 10, display_min_rows: int = 25, display_width: int = 320, from_csv: bool | str = False, info_dic: dict = None)[source]¶

Creates an object from binance klines and/or trade data. It contains the raw api response, a dataframe that can be modified and many more.

Symbols can be any trading pair on Binance, such as BTCUSDT or ETHBUSD, and time intervals can be specified using the following strings:

` '1m', '3m', '5m', '15m', '30m', '1h', '2h', '4h', '6h', '8h', '12h', '1d', '3d', '1w', or '1M' `The class provides several plotting methods for quick data visualization.

- Parameters:

symbol (str) – It can be any symbol in the binance exchange, like BTCUSDT, ethbusd or any other. Capital letters don’t matter.

tick_interval (str) – Any candle’s interval available in binance. Capital letters don’t matter.

It can be an integer in milliseconds from epoch (1970-01-01 00:00:00 UTC) or any string in the formats:

- %Y-%m-%d %H:%M:%S.%f: **2022-05-11 06:45:42.124567** - %Y-%m-%d %H:%M:%S: **2022-05-11 06:45:42**

If start time is passed, it gets the next open according to the tick interval selected except an exact open time passed.

It can be an integer in milliseconds from epoch (1970-01-01 00:00:00 UTC) or any string in the formats:

- %Y-%m-%d %H:%M:%S.%f: **2022-05-11 06:45:42.124** - %Y-%m-%d %H:%M:%S: **2022-05-11 06:45:42**

If end time is passed, it gets candles till the previous close according to the selected tick interval.

Example with daily time saving inside the interval:

import binpan btcusdt = binpan.Symbol(symbol='btcusdt', tick_interval='15m', time_zone='Europe/Madrid', start_time='2021-10-31 01:00:00', end_time='2021-10-31 03:00:00') btcusdt.df Open High Low Close Volume BTCUSDT 15m Europe/Madrid 2021-10-31 01:00:00+02:00 61540.32 61780.44 61488.35 61737.39 316.93504 2021-10-31 01:15:00+02:00 61737.39 61748.13 61486.86 61637.99 485.50681 2021-10-31 01:30:00+02:00 61637.99 61777.71 61479.76 61743.32 441.29718 2021-10-31 01:45:00+02:00 61743.31 61900.00 61640.55 61859.19 505.87893 2021-10-31 02:00:00+02:00 61859.19 62328.38 61859.18 62328.13 1046.30598 2021-10-31 02:15:00+02:00 62328.13 62399.00 62142.74 62246.30 679.96187 2021-10-31 02:30:00+02:00 62246.30 62371.72 62171.01 62301.39 355.25273 2021-10-31 02:45:00+02:00 62301.39 62400.15 62220.27 62375.29 568.02797 2021-10-31 02:00:00+01:00 62375.28 62405.30 62260.01 62367.79 421.52566 2021-10-31 02:15:00+01:00 62367.79 62394.06 62219.50 62270.00 537.53843 2021-10-31 02:30:00+01:00 62270.00 62371.49 62156.83 62169.01 452.62728 2021-10-31 02:45:00+01:00 62169.01 62227.00 62114.18 62169.00 283.45948

limit (int) –

The limit is the quantity of candles requested. Can combine with start_time or end_time:

If no start or end timestamp passed, gets current timestamp and limit of candles backwards.

If just start time or endtime passed, then applies the limit to find the endtime or start time respectively.

if endtime and start time passed, it gets all the ticks between, even if more than 1000 by calling several times to API until completed. Limit ignored.

time_zone (str) –

The index of the pandas dataframe in the object can be converted to any timezone, i.e. “Europe/Madrid”

The binance API use milliseconds from epoch (1970-01-01 00:00:00 UTC), that means that converting to a timezoned date with daily time saving changes, the result would show the change in the timestamp.

Candles are ordered with the timestamp regardless of the index name, even if the index shows the hourly change because daily time saving changes.

closed (bool) – The last candle is a closed one in the moment of the creation, discarding the current running one not closed yet. Default True.

display_columns (int) – Number of columns in the dataframe display. Convenient to adjust in jupyter notebooks.

display_max_rows (int) – Number of rows in the dataframe display. Convenient to adjust in jupyter notebooks.

display_width (int) – Display width in the dataframe display. Convenient to adjust in jupyter notebooks.

display_min_rows (int) – Number of rows in the dataframe display. Convenient to adjust in jupyter notebooks.

postgres_klines (bool or str) – If True, gets data from a postgres database by selecting interactively from tables found. Also a string with table name can be used. If str passed, it will be used as host.

postgres_agg_trades (bool) – If True, gets data from a postgres database by selecting interactively from tables found. Also a string with table name can be used. If str passed, it will be used as host.

postgres_atomic_trades (bool) – If True, gets data from a postgres database by selecting interactively from tables found. Also a string with table name can be used. If str passed, it will be used as host.

binbase (bool or str) – If True, gets data from binbase TimescaleDB (shared schema with symbol column). If str passed, it will be used as host. Password from

BINBASE_PASSWORDenv var or panzer’sbinbase_password(~/.panzer_creds).hours (float) – If hours is passed, it gets the candles from the last hours.

from_csv (bool or str) – If True, gets data from a csv file by selecting interactively from csv files found. Also a string with filename can be used.

info_dic (dict) – Sometimes, for iterative processes, info_dic can be passed to avoid calling API for it. Its weight is heavy.

from_csv – If True, gets data from a csv file by selecting interactively from csv files found. Also a string with filename can be used.

info_dic – Sometimes, for iterative processes, info_dic can be passed to avoid calling API for it. Its weight is heavy.

Examples:

binpan_object = binpan.Symbol(symbol='ethbusd', tick_interval='5m', limit=100, display_rows=10) binpan_object.df Open High Low Close Volume Quote volume Trades Taker buy base volume Taker buy quote volume ETHBUSD 5m UTC 2022-06-22 08:55:00+00:00 1077.29 1081.11 1076.34 1080.18 810.1562 8.737861e+05 1401.0 410.0252 4.422960e+05 2022-06-22 09:00:00+00:00 1080.28 1087.31 1079.90 1085.03 2446.4199 2.653134e+06 3391.0 1253.6380 1.359514e+06 2022-06-22 09:05:00+00:00 1085.14 1085.98 1080.70 1080.99 1502.4415 1.628110e+06 1664.0 509.9937 5.525626e+05 2022-06-22 09:10:00+00:00 1080.79 1084.53 1080.26 1083.30 906.5092 9.814984e+05 1438.0 514.6718 5.573028e+05 2022-06-22 09:15:00+00:00 1083.42 1085.35 1081.41 1081.53 1191.9566 1.291633e+06 1549.0 736.5743 7.983178e+05 ... ... ... ... ... ... ... ... ... ... 2022-06-22 16:50:00+00:00 1067.61 1070.00 1066.21 1069.32 1951.1378 2.084288e+06 1535.0 1396.4956 1.491744e+06 2022-06-22 16:55:00+00:00 1069.47 1078.61 1069.47 1077.78 2363.1639 2.539150e+06 3578.0 1239.7735 1.332085e+06 2022-06-22 17:00:00+00:00 1077.96 1079.32 1071.25 1073.00 1452.3712 1.560748e+06 2534.0 651.9175 7.006751e+05 2022-06-22 17:05:00+00:00 1072.76 1075.04 1071.00 1073.47 728.9761 7.820787e+05 1383.0 303.3896 3.254396e+05 2022-06-22 17:10:00+00:00 1073.42 1076.30 1073.24 1075.77 228.4269 2.456515e+05 426.0 127.7424 1.373634e+05 100 rows × 9 columns

Methods:

save_csv([timestamped_filename])Saves current klines DataFrame to a csv file.

save_atomic_trades_csv([timestamped_filename])Saves current atomic trades to a csv file.

save_agg_trades_csv([timestamped_filename])Saves current aggregated trades to a csv file.

set_display_max_columns([display_columns])Method to change the maximum number of columns shown in the display of the dataframe.

set_display_min_rows([display_min_rows])Method to change the number of minimum rows shown in the display of the dataframe.

set_display_max_rows([display_max_rows])Method to change the number of maximum rows shown in the display of the dataframe.

set_display_width([display_width])Method to change the width shown in the display of the dataframe.

set_display_decimals(display_decimals)Method to change the number of decimals shown in the display of the dataframe.

basic([exceptions, actions_col])Shows just a basic selection of columns data in the dataframe.

drop([columns_to_drop, inplace])It drops some columns from the dataframe.

delete_indicator_family(indicator_name_root)Deletes indicator from dataframe.

insert_indicator(source_data[, ...])Adds one or more indicators to the DataFrame in place.

hk([inplace])It computes Heikin Ashi candles.

Get the first Open timestamp and the last Open timestamp.

Get the first Open timestamp and the last Open timestamp, and converts to timezoned dates.

get_agg_trades([hours, minutes, startTime, ...])Calls the API and creates another dataframe included in the object with the aggregated trades from API for the period of the created object.

get_atomic_trades([hours, minutes, ...])Calls the API and creates another dataframe included in the object with the atomic trades from API for the period of the created object.

is_new(source_data[, suffix])Verify if indicator columns are previously created to avoid allocating new rows and colors etc.

get_reversal_agg_candles([min_height, ...])Resamples aggregated API trades to reversal klines:

get_reversal_atomic_candles([min_height, ...])Resamples API atomic trades to reversal klines:

resample(tick_interval[, inplace])Resample trades to a different tick interval.

Repair kline discontinuities by filling missing candles.

accumulation_distribution([inplace, suffix, ...])Accumulation/Distribution indicator.

alternating_fractal([max_period, inplace, ...])Obtains the minim value for fractal_w periods as fractal is pure alternating from max to min to max etc.

atr([length, inplace, suffix, color])Average True Range.

backtesting(actions_col[, target_column, ...])Simulates buys and sells using labels in a tagged column with actions.

bbands([length, std, ddof, inplace, suffix, ...])These bands consist of an upper Bollinger band and a lower Bollinger band and are placed two standard deviations above and below a moving average.

cci([length, scaling, inplace, suffix, color])Compute the Commodity Channel Index (CCI) for NIFTY based on the 14-day moving average.

clean_in_out(column[, in_tag, out_tag, ...])It cleans a serie with in and out tags by eliminating in streaks and out streaks.

cross(slow[, fast, cross_over_tag, ...])It tags crossing values from a column/serie (fast) over a serie or value (slow).

ema([window, column, inplace, suffix, color])Generate technical indicator Exponential Moving Average.

eom([length, divisor, drift, inplace, ...])Ease of Movement (EMV) can be used to confirm a bullish or a bearish trend.

ffill_window(column[, window, inplace, ...])It forward fills a value through nans a window ahead.

fractal([period, inplace, overlap_plot, ...])The fractal indicator is based on a simple price pattern that is frequently seen in financial markets.

get_maker_taker_buy_ratios([window, ...])Generates the makers versus makers+takers volume ratio by each_kline.

get_market_profile([bins, hours, minutes, ...])Generates a market profile dataframe from trade or kline data.

Returns column names starting with "Strategy".

get_taker_maker_ratio_profile([bins, hours, ...])Generates a market profile of the makers versus makers+takers volume ratio by each_kline.

ichimoku([tenkan, kijun, chikou_span, ...])The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction.

ma([ma_name, column_source, inplace, ...])Generic moving average method.

macd([fast, slow, smooth, inplace, suffix, ...])Generate technical indicator Moving Average, Convergence/Divergence (MACD).

merge_columns(main_column, other_column[, ...])Predominant serie will be filled nans with values, if existing, from the other serie.

on_balance_volume([inplace, suffix, color])On balance indicator.

pandas_ta_indicator(name, **kwargs)Calls any indicator in pandas_ta library with function name as first argument and any kwargs the function will use.

plot([width, height, ...])Plots a candles figure for the object.

plot_agg_trades_size([max_size, height, ...])It plots a time series graph plotting aggregated trades sized by quantity and color if taker or maker buyer.

plot_aggression_sizes([bins, hist_funct, ...])Binance fees can be cheaper for maker orders, many times when big traders, like whales, are operating .

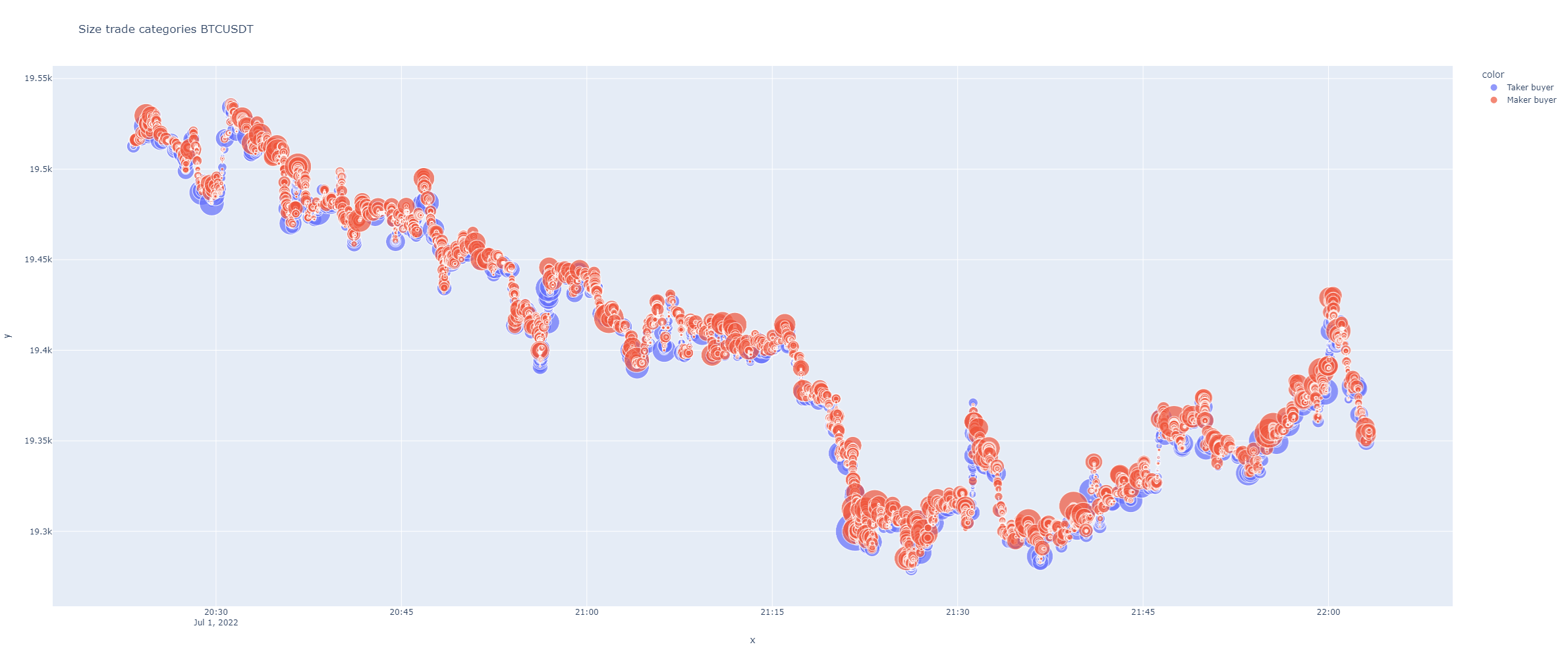

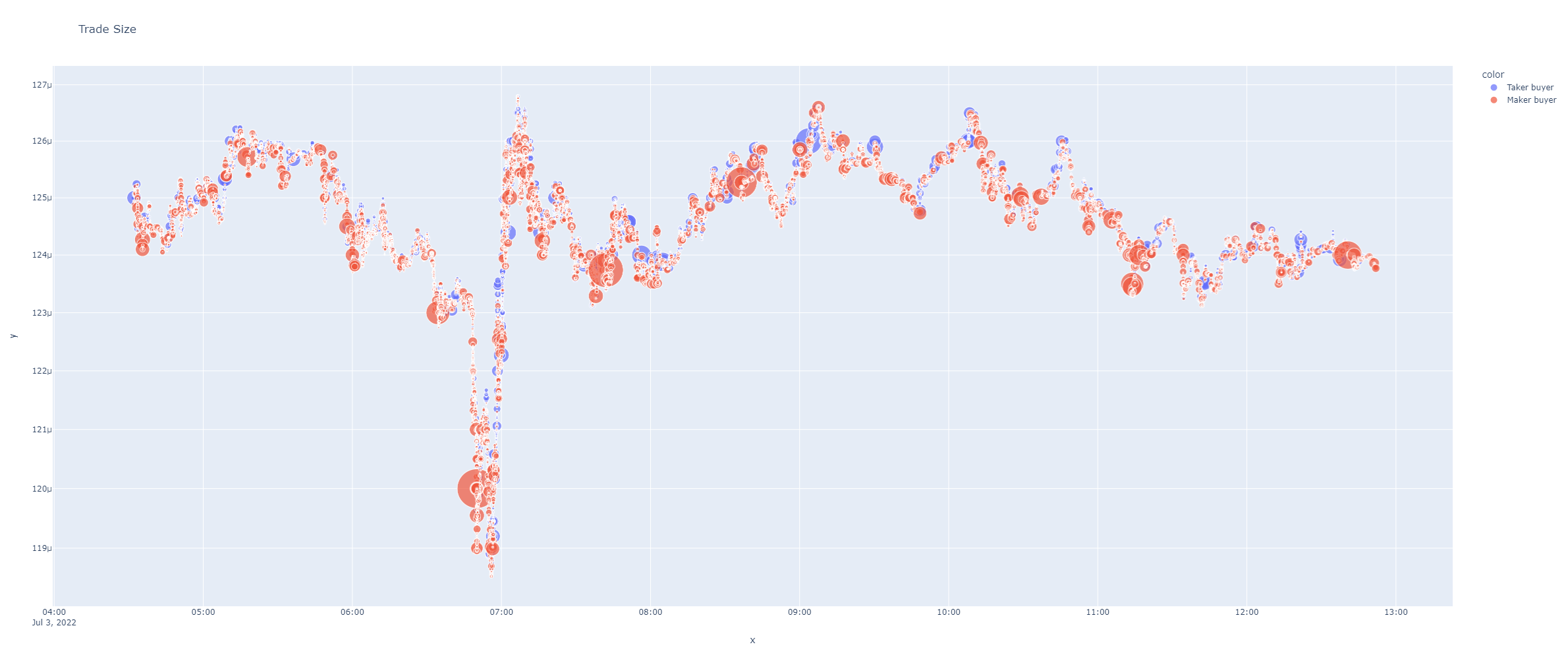

plot_atomic_trades_size([max_size, height, ...])It plots a time series graph plotting atomic trades sized by quantity and color if taker or maker buyer.

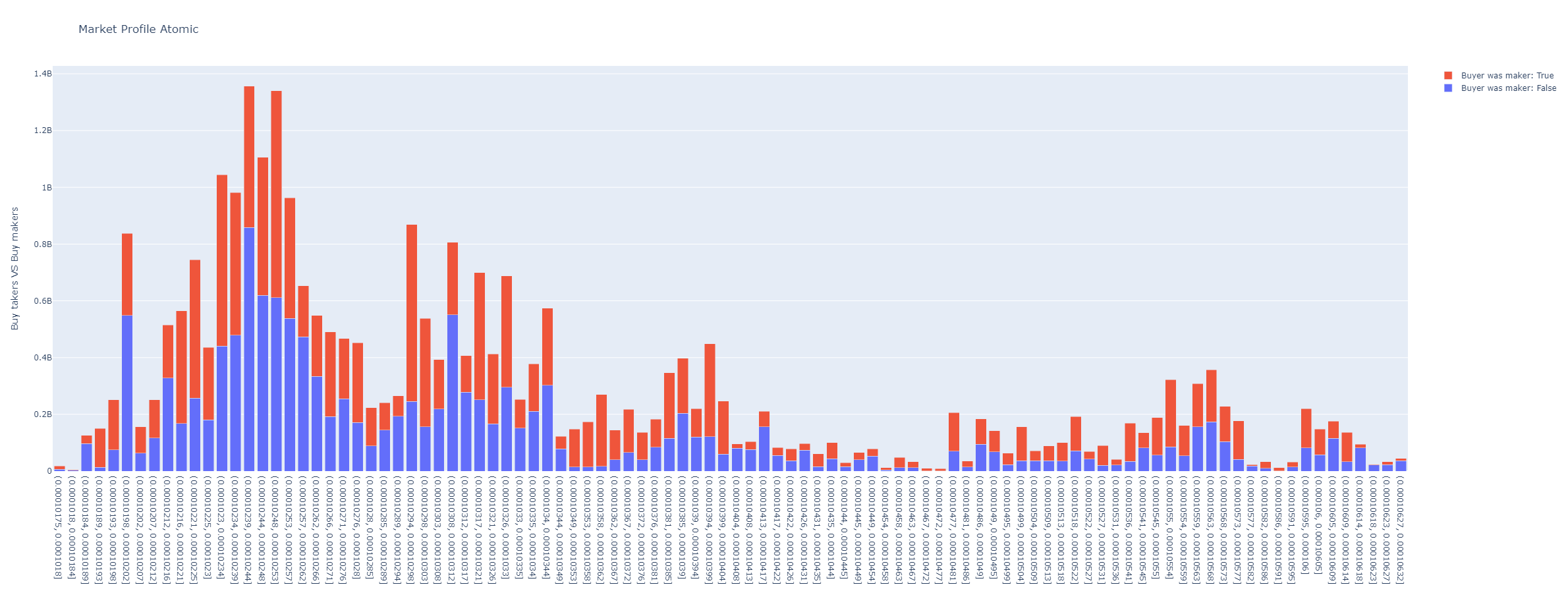

plot_market_profile([bins, hours, minutes, ...])Plots volume histogram by prices segregated aggressive buyers from sellers.

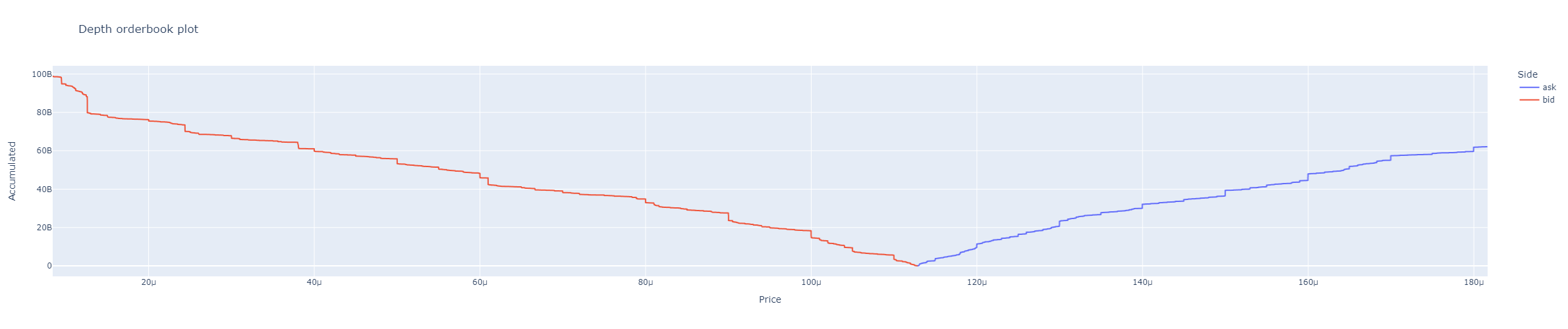

plot_orderbook([accumulated, title, height, ...])Plots orderbook depth.

plot_orderbook_density([x_col, color, bins, ...])Plot a distribution plot for a dataframe column.

plot_reversal([min_height, min_reversal, ...])Plots reversal candles.

plot_taker_maker_ratio_profile([bins, ...])Plots taker vs maker ratio profile.

plot_trades_pie([categories, logarithmic, title])Plots a pie chart.

plot_trades_scatter([x, y, dot_symbol, ...])A scatter plot showing each price level volume or trades.

plot_volume_profile([bins, value_area_pct, ...])Volume Profile (VPVR): velas + histograma horizontal de volumen, con POC y Value Area.

profit_hour([column])It returns win or loos quantity per hour.

remove_plot_info_associated_columns(columns, ...)Completely remove plot info for a column in main dataframe of klines.

remove_plot_info_for_column(column)Remove plot info for a column in main dataframe of klines.

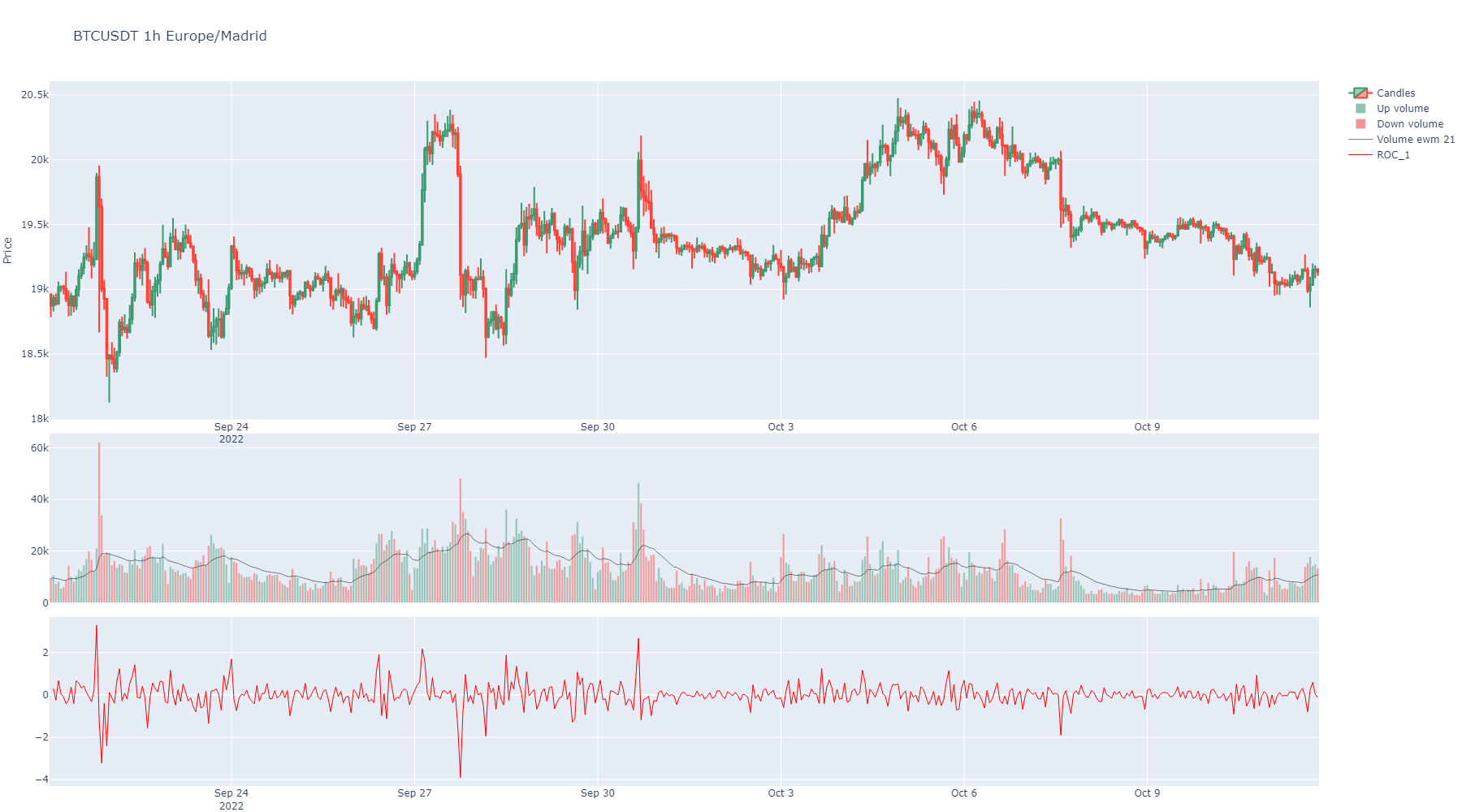

roc([length, escalar, inplace, suffix, color])The Rate of Change (ROC) is a technical indicator that measures the percentage change between the most recent price and the price "n" day's ago.

roi([column])It returns win or loos percent for a evaluation column.

rolling_support_resistance([minutes_window, ...])Calculate support and resistance levels for the Symbol based on either atomic trades or aggregated trades in a rolling window.

rsi([length, inplace, suffix, color])Relative Strength Index (RSI).

set_plot_axis_group([indicator_column, ...])Internal control formatting plots.

set_plot_color([indicator_column, color])Internal control formatting plots.

set_plot_color_fill([indicator_column, ...])Internal control formatting plots.

set_plot_filled_mode([indicator_column, ...])Internal control formatting plots.

set_plot_row([indicator_column, row_position])Internal control formatting plots.

Modify the control for splitted series in plots with colored area in two colors by relative position.

set_plotting_volume_ma([window])Set a window for plotting volume moving average on the candles plot when volumen bars are plotted.

set_strategy_groups(column, group[, ...])Returns strategy_groups for BinPan DataFrame.

shift(column[, window, strategy_group, ...])It shifts a candle ahead by the window argument value (or backwards if negative)

sma([window, column, inplace, suffix, color])Generate technical indicator Simple Moving Average.

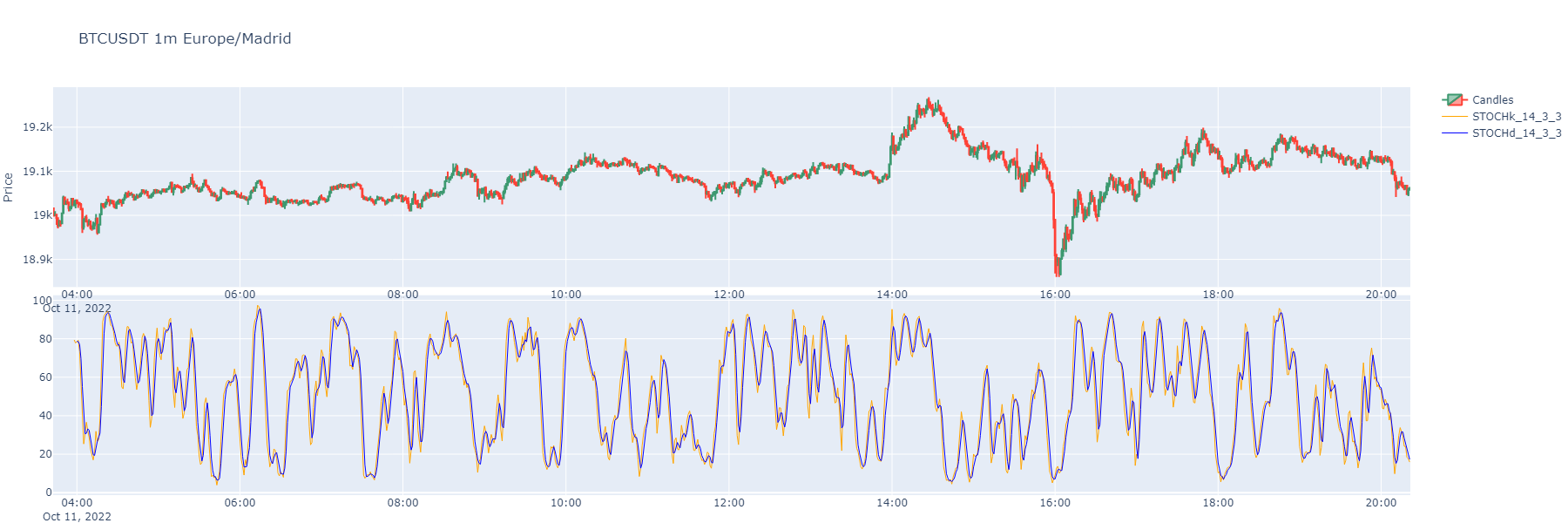

stoch([k_length, stoch_d, k_smooth, ...])Stochastic Oscillator with a fast and slow exponential moving averages.

stoch_rsi([rsi_length, k_smooth, d_smooth, ...])Stochastic Relative Strength Index (RSI) with a fast and slow exponential moving averages.

strategy_from_tags_crosses([columns, ...])Checks where all tags and cross columns get value "1" at the same time.

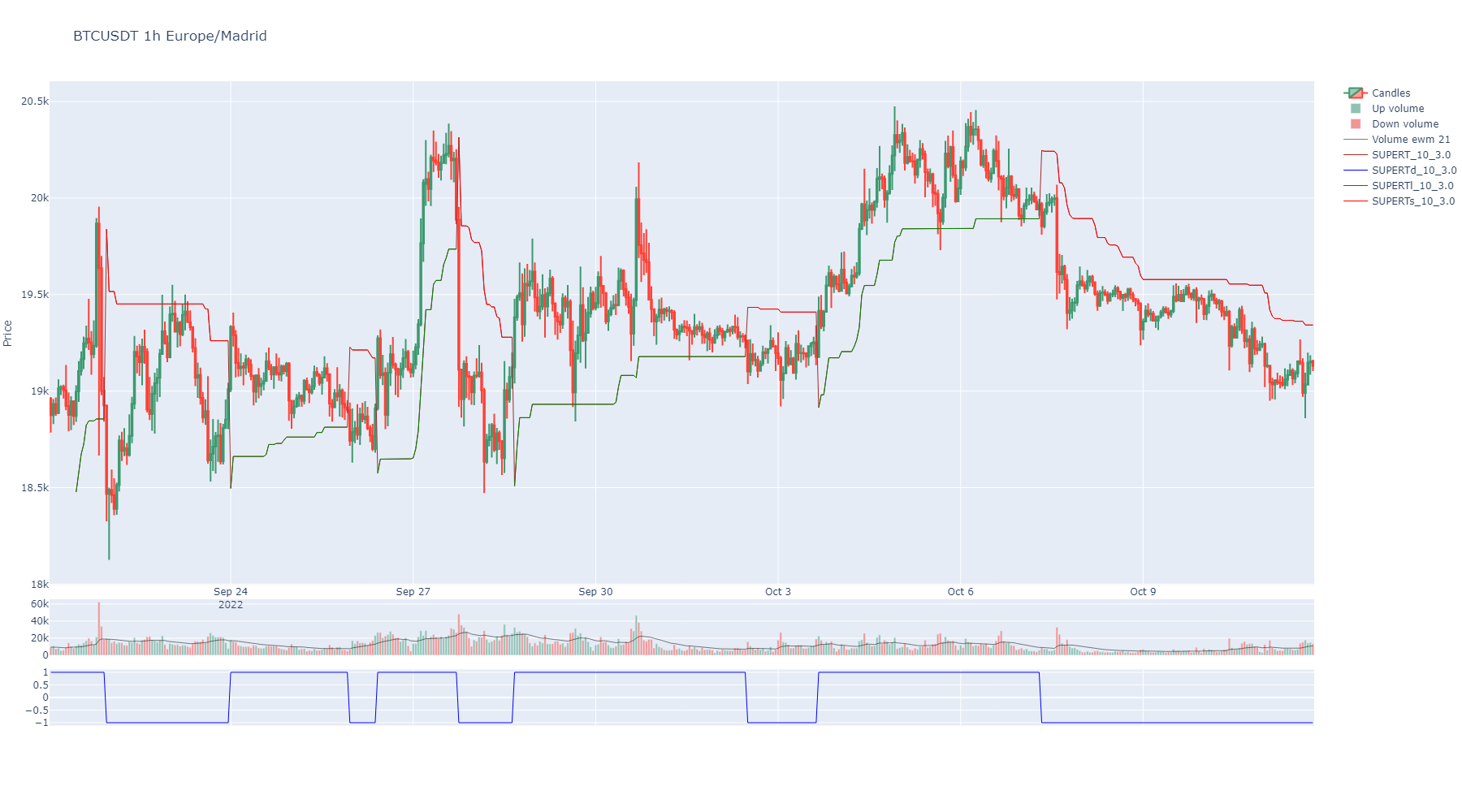

supertrend([length, multiplier, inplace, ...])Generate technical indicator Supertrend.

support_resistance([from_atomic, ...])Calculate support and resistance levels for the Symbol based on either atomic trades or aggregated trades.

tag(column, reference[, relation, ...])It tags values of a column/serie compared to other serie or value by methods gt,ge,eq,le,lt as condition.

time_centroids([from_atomic, ...])Calculate centroids for timestamps of more activity in taker buys or takers sells.

Returns exchangeInfo data when instantiated.

volume_profile([bins, value_area_pct, ...])Volume Profile (VPVR): volumen por nivel de precio + POC, Value Area y nodos HVN/LVN.

vwap([anchor, inplace, suffix, color])Volume Weighted Average Price.

Get exchange info about the symbol for order filters.

Get exchange info about the symbol for order types.

Get exchange info about the symbol for trading permissions.

Get exchange info about the symbol for assets precision.

Return the symbol status, TRADING, BREAK, etc.

get_fees([symbol])Shows applied fees for the symbol of the object.

get_orderbook([limit])Gets orderbook.

- save_csv(timestamped_filename: bool = True) None[source]¶

Saves current klines DataFrame to a csv file.

- Parameters:

timestamped_filename (bool) – Adds start and end timestamps to the name.

- Returns:

None

- save_atomic_trades_csv(timestamped_filename: bool = True) None[source]¶

Saves current atomic trades to a csv file.

- Parameters:

timestamped_filename (bool) – Adds start and end timestamps to the name.

- Returns:

None

- save_agg_trades_csv(timestamped_filename: bool = True) None[source]¶

Saves current aggregated trades to a csv file.

- Parameters:

timestamped_filename (bool) – Adds start and end timestamps to the name.

- Returns:

None

- set_display_max_columns(display_columns=None) None[source]¶

Method to change the maximum number of columns shown in the display of the dataframe. Uses pandas options.

- Parameters:

display_columns (int) – Integer

- Returns:

None

- set_display_min_rows(display_min_rows=None) None[source]¶

Method to change the number of minimum rows shown in the display of the dataframe. Uses pandas options.

- Parameters:

display_min_rows (int) – Integer

- set_display_max_rows(display_max_rows=None) None[source]¶

Method to change the number of maximum rows shown in the display of the dataframe. Uses pandas options.

- Parameters:

display_max_rows (int) – Integer

- set_display_width(display_width: int = None) None[source]¶

Method to change the width shown in the display of the dataframe. Uses pandas options.

- Parameters:

display_width (int) – Integer

- static set_display_decimals(display_decimals: int) None[source]¶

Method to change the number of decimals shown in the display of the dataframe. Uses pandas options.

- Parameters:

display_decimals (int) – Integer

- basic(exceptions: list = None, actions_col='actions') DataFrame[source]¶

Shows just a basic selection of columns data in the dataframe.

- drop(columns_to_drop=None, inplace=False) DataFrame[source]¶

It drops some columns from the dataframe. If columns list not passed, then defaults to the initial columns.

Can be used when messing with indicators to clean the object.

- Param:

list columns: A list with the columns names to drop. If not passed, it defaults to the initial columns that remain from when instanced. Defaults to any column but initial ones.

- Param:

bool inplace: When true, it drops columns in the object. False just returns a copy without that columns and dataframe in the object remains.

- Return pd.DataFrame:

Pandas DataFrame with columns dropped.

- delete_indicator_family(indicator_name_root: str) DataFrame | None[source]¶

Deletes indicator from dataframe. It search for plot info and also deletes other indicators in the same plot row level.

- Parameters:

indicator_name_root (str) – Starting characters for the columns to delete. Case-insensitive.

- Returns:

Resulting main dataframe.

- insert_indicator(source_data: Series | DataFrame | ndarray | list, strategy_group: str | None = None, plotting_row: int | None = None, plotting_rows: list[int] | None = None, color: str | None = None, no_overlapped_plot_rows: bool = True, colors: list[str] | None = None, color_fills: list[str | bool] | None = None, name: str | None = None, names: list[str] | None = None, suffix: str = '') DataFrame | None[source]¶

Adds one or more indicators to the DataFrame in place.

- Parameters:

source_data – The source data for the indicator(s). Can be a Series, DataFrame, ndarray, or list thereof.

strategy_group – (Optional) Name of the strategy group to tag the inserted data.

plotting_row – (Optional) The specific row for plotting a single series. ‘1’ overlaps with candles; other values create new rows.

plotting_rows – (Optional) List of rows for plotting each series. ‘1’ means overlap; other integers determine separate row positions.

color – (Optional) Color for plotting a single series.

no_overlapped_plot_rows – If True, avoids overlapping plot rows for multiple series.

colors – (Optional) List of colors for each series indicator. Defaults to random colors if not provided.

color_fills – (Optional) List of color fills (as strings) or False to avoid filling. Example: ‘rgba(26,150,65,0.5)’.

name – (Optional) Name for a single inserted object.

names – (Optional) List of names for each column when multiple indicators are inserted.

suffix – Suffix to add to the new column name(s). If the source data is nameless, the suffix becomes the entire name.

- Returns:

The modified DataFrame with new indicators added, or None if the operation fails.

Note: This function dynamically assigns plotting rows and colors if they are not explicitly provided. It handles different types of input data for indicators and integrates them into the existing DataFrame.

- hk(inplace=False) DataFrame[source]¶

It computes Heikin Ashi candles. Any existing indicator column will not be recomputed. It is recommended to drop any indicator before converting candles to Heikin Ashi.

- Parameters:

inplace (bool) – Change object dataframe permanently whe True is selected. False shows a copy dataframe.

- Return pd.DataFrame:

Pandas DataFrame

- get_timestamps() tuple[int, int][source]¶

Get the first Open timestamp and the last Open timestamp.

- Return tuple[int, int]:

Tuple of (start_ms, end_ms) open timestamps.

- get_dates() tuple[str, str][source]¶

Get the first Open timestamp and the last Open timestamp, and converts to timezoned dates.

- Return tuple[str, str]:

Tuple of (start_date, end_date) as formatted strings.

- get_agg_trades(hours: int = None, minutes: int = None, startTime: int | str = None, endTime: int | str = None, time_zone: str = None, from_csv: str = None) Trades[source]¶

Calls the API and creates another dataframe included in the object with the aggregated trades from API for the period of the created object.

Note

If the object covers a long time interval, this action can take a relative long time. The BinPan library take care of the API weight and can take a sleep to wait until API weight returns to a low value. This avoids ban from the API.

- Parameters:

hours (int) – If passed, it use just last passed hours for the plot.

minutes (int) – If passed, it use just last passed minutes for the plot.

startTime (int or str) – If passed, it use just from the timestamp or date in format (%Y-%m-%d %H:%M:%S: 2022-05-11 06:45:42)) for the plot.

endTime (int or str) – If passed, it use just until the timestamp or date in format (%Y-%m-%d %H:%M:%S: 2022-05-11 06:45:42)) for the plot.

time_zone (str) – A time zone for time index conversion. Example: “Europe/Madrid”

from_csv (str) – If set, loads from a file.

- Returns:

Pandas DataFrame

- get_atomic_trades(hours: int = None, minutes: int = None, startTime: int | str = None, endTime: int | str = None, time_zone: str = None, from_csv: str = None) Trades[source]¶

Calls the API and creates another dataframe included in the object with the atomic trades from API for the period of the created object.

Note

If the object covers a long time interval, this action can take a relative long time. The BinPan library take care of the API weight and can take a sleep to wait until API weight returns to a low value.

- Parameters:

hours (int) – If passed, it use just last passed hours for the plot.

minutes (int) – If passed, it use just last passed minutes for the plot.

startTime (int or str) – If passed, it use just from the timestamp or date in format (%Y-%m-%d %H:%M:%S: 2022-05-11 06:45:42)) for the plot.

endTime (int or str) – If passed, it use just until the timestamp or date in format (%Y-%m-%d %H:%M:%S: 2022-05-11 06:45:42)) for the plot.

time_zone (str) – A time zone for time index conversion. Example: “Europe/Madrid”

from_csv (str) – If set, loads from a file.

- Returns:

Pandas DataFrame

- is_new(source_data: Series | DataFrame, suffix: str = '') bool[source]¶

Verify if indicator columns are previously created to avoid allocating new rows and colors etc.

- Parameters:

source_data (pd.Series or pd.DataFrame) – Data from pandas_ta to review if is previously computed.

suffix (str) – If suffix passed, it takes it into account when searching for existence.

- Return bool:

- get_reversal_agg_candles(min_height: int = 7, min_reversal: int = 4) DataFrame | None[source]¶

- Resamples aggregated API trades to reversal klines:

- Parameters:

min_height – Defaults to 7. Minimum reversal kline height to close a candle

min_reversal – Defaults to 4. Minimum reversal from hig/low to close a candle

- Return pd.DataFrame:

Resample trades to reversal klines. Can be plotted.

- get_reversal_atomic_candles(min_height: int = 7, min_reversal: int = 4) DataFrame | None[source]¶

- Resamples API atomic trades to reversal klines:

- Parameters:

min_height – Defaults to 7. Minimum reversal kline height to close a candle

min_reversal – Defaults to 4. Minimum reversal from hig/low to close a candle

- Return pd.DataFrame:

Resample trades to reversal klines. Can be plotted.

- resample(tick_interval: str, inplace=False) DataFrame | None[source]¶

Resample trades to a different tick interval. Tick interval must be higher. :param str tick_interval: A binance tick interval. Must be higher than current tick interval. :param bool inplace: Change object dataframe permanently whe True is selected. False shows a copy dataframe. :return pd.DataFrame: Resampled klines.

- repair_continuity() None[source]¶

Repair kline discontinuities by filling missing candles.

Updates the instance DataFrame in place and re-checks continuity.

- accumulation_distribution(inplace: bool = True, suffix: str = '', color: str | int = None, **kwargs) Series¶

Accumulation/Distribution indicator.

- Parameters:

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

color (str or int) – Is the color to show when plotting or index in that list.

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/volume/ad.py

- Returns:

A Pandas Series

- alternating_fractal(max_period: int = None, inplace: bool = True, overlap_plot=True, with_trend: bool = True, suffix: str = '', colors: list = None) tuple[Series | None, float | None, float | None]¶

Obtains the minim value for fractal_w periods as fractal is pure alternating from max to min to max etc. In other words, max and mins alternates in regular rhythm without any tow max or two mins consecutively.

This custom indicator shows the minimum period in finding a pure alternating fractal. It is some kind of rhythm in price indicator, the most period needed, the slow price rhythm.

- Parameters:

max_period (int) – Default is len of dataframe. This method will check from 2 to the max period value to find a alternating max to mins.

inplace (bool) – Make it permanent in the instance or not.

overlap_plot (bool) – If True, it will overlap the indicator plot with the price plot.

with_trend (bool) – If true, it will return maximums diff mean and minimums diff mean also.

suffix (str) – A decorative suffix for the name of the column created.

colors (list) – A list of colors for the indicator dataframe columns. Is the color to show when charts. It can be any color from plotly library or a number in the list of those. Default colors defined. https://community.plotly.com/t/plotly-colours-list/11730

- Return pd.DataFrame:

A dataframe with two columns, one with 1 or -1 for local max or local min to tag, and other with price values for that points. Alternatively, maximums and minimums diff mean will be returned.

- atr(length: int = 14, inplace: bool = True, suffix: str = '', color: str | int = None, **kwargs) Series¶

Average True Range.

- Parameters:

length (str) – Window period to obtain ATR. Default is 14.

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

color (str or int) – Is the color to show when plotting or index in that list.

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/volatility/atr.py

- Returns:

A Pandas Series

- backtesting(actions_col: str | int, target_column: str | Series = None, stop_loss_column: str | Series = None, entry_filter_column: str | Series = None, fixed_target: bool = True, fixed_stop_loss: bool = True, base: float = 0, quote: float = 1000, priced_actions_col: str = 'Open', label_in=1, label_out=-1, fee: float = 0.001, evaluating_quote: str = None, short: bool = False, inplace=True, suffix: str = None, colors: list = None) DataFrame | Series¶

Simulates buys and sells using labels in a tagged column with actions. Actions are considered before the tag, in the next candle using priced_actions_col price of that candle before.

- Parameters:

target_column – Column with data for operation target values.

stop_loss_column – Column with data for operation stop loss values.

entry_filter_column (pd.Series | str) – A serie or colum with ones or zeros to allow or avoid entries.

fixed_target (bool) – Target for any operation will be calculated and fixed at the beginning of the operation.

fixed_stop_loss (bool) – Stop loss for any operation will be calculated and fixed at the beginning of the operation.

base (float) – Base inverted quantity.

quote (float) – Quote inverted quantity.

priced_actions_col (str | int) – Columna name or index with prices to use when action label in a row.

label_in (str | int) – A label consider as trade in trigger.

label_out (str | int) – A label consider as trade out trigger.

fee (float) – Fees applied to the simulation.

evaluating_quote (str) – A quote used to convert value of the backtesting line for better reference.

short (bool) – Backtest in short mode, with in as shorts and outs as repays.

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

colors (list) – Defaults to red and green.

- Return pd.DataFrame | pd.Series:

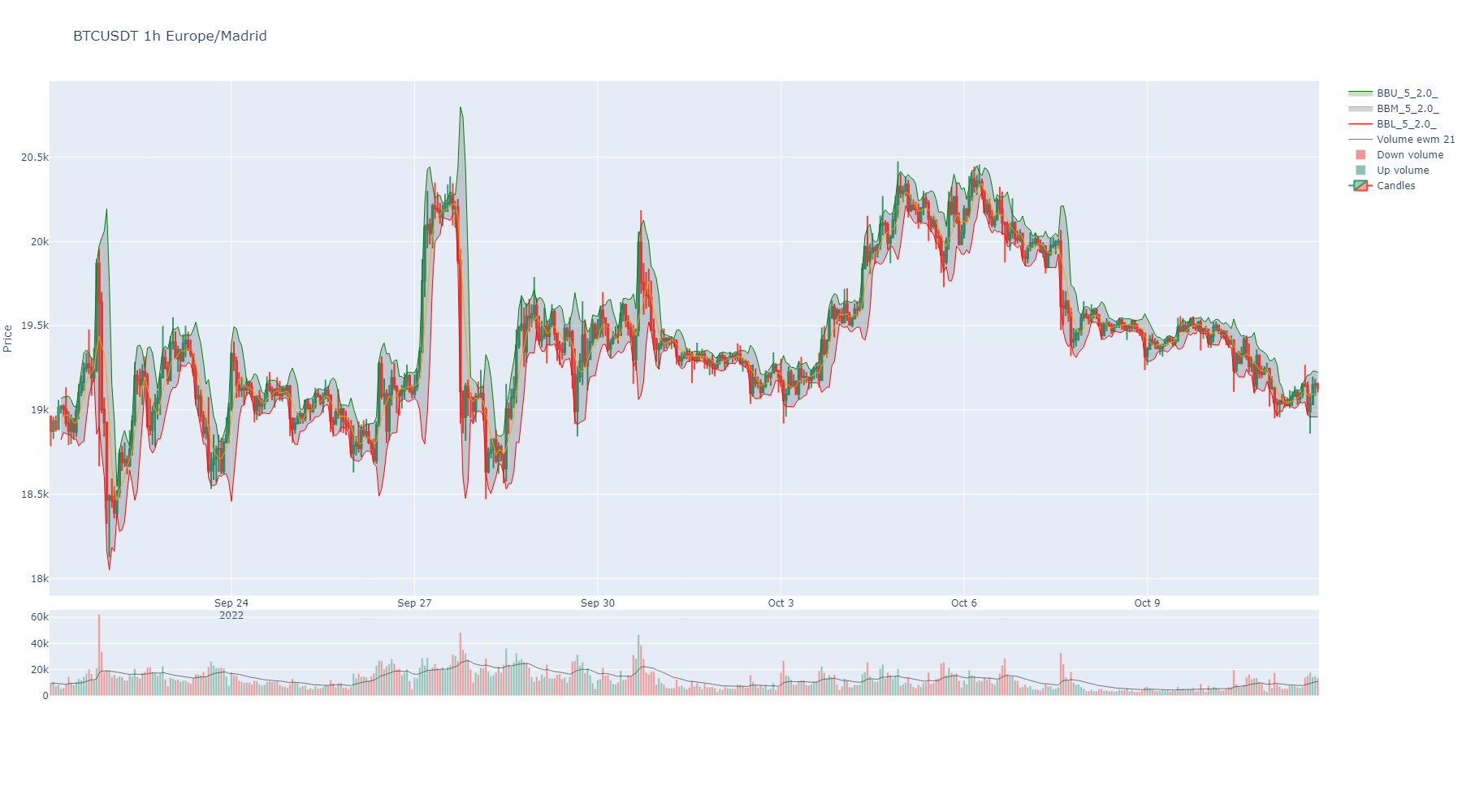

- bbands(length: int = 5, std: int = 2, ddof: int = 0, inplace: bool = True, suffix: str = '', colors: list = None, my_fill_color: str = 'rgba(47, 48, 56, 0.2)', **kwargs) DataFrame¶

These bands consist of an upper Bollinger band and a lower Bollinger band and are placed two standard deviations above and below a moving average. Bollinger bands expand and contract based on the volatility. During a period of rising volatility, the bands widen, and they contract as the volatility decreases. Prices are considered to be relatively high when they move above the upper band and relatively low when they go below the lower band.

- Parameters:

length (int) – The short period. Default: 5

std (int) – The long period. Default: 2

ddof (int) – Degrees of Freedom to use. Default: 0

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

colors (list) – A list of colors for the indicator dataframe columns. Is the color to show when charts. It can be any color from plotly library or a number in the list of those. Default colors defined. https://community.plotly.com/t/plotly-colours-list/11730

my_fill_color (str) – An rgba color code to fill between bands area. https://rgbacolorpicker.com/

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/volatility/bbands.py

- Returns:

pd.Series

- cci(length: int = 14, scaling: int = None, inplace: bool = True, suffix: str = '', color: str | int = None, **kwargs) Series¶

Compute the Commodity Channel Index (CCI) for NIFTY based on the 14-day moving average. CCI can be used to determine overbought and oversold levels.

Readings above +100 can imply an overbought condition

Readings below −100 can imply an oversold condition.

However, one should be careful because security can continue moving higher after the CCI indicator becomes overbought. Likewise, securities can continue moving lower after the indicator becomes oversold.

- Parameters:

length (str) – Window period to obtain ATR. Default is 14.

scaling (str) – Scaling Constant. Default: 0.015.

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

color (str or int) – Is the color to show when plotting or index in that list.

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/momentum/cci.py

- Returns:

A Pandas Series

- clean_in_out(column: str | int | Series, in_tag=1, out_tag=-1, strategy_group: str = '', inplace=True, suffix: str = '', color: str | int = 'grey') Series¶

It cleans a serie with in and out tags by eliminating in streaks and out streaks.

Same kind of index needed.

- Parameters:

column (pd.Series) – A column to clean in and out values.

in_tag – Tag for in tags. Default is 1.

out_tag – Tag for out tags. Default is -1.

strategy_group (str) – A name for a group of columns to assign to a strategy.

inplace (bool) – Permanent or not. Default is false, because of some testing required sometimes.

suffix (str) – A string to decorate resulting Pandas series name.

color (str | int) – A color from plotly list of colors or its index in that list.

- Return pd.Series:

A merged serie.

- cross(slow: str | int | float | Series, fast: str | int | Series = 'Close', cross_over_tag: str | int = 1, cross_below_tag: str | int = -1, echo=0, non_zeros: bool = True, strategy_group: str = None, inplace=True, suffix: str = '', color: str | int = 'green') Series¶

It tags crossing values from a column/serie (fast) over a serie or value (slow).

- Parameters:

slow (pd.Series | str | int | float) – A number or numeric serie or column name.

fast (pd.Series | str) – A numeric serie or column name or column index. Default is Close price.

cross_over_tag (int | str) – Value or string to tag matched crossing fast over slow.

cross_below_tag (int | str) – Value or string to tag crossing slow over fast.

non_zeros (bool) – Result will not contain zeros as non tagged values, instead will be nans.

echo (int) – It tags a fixed amount of candles forward the crossed point not including cross candle. If echo want to be used, must be used non_zeros.

strategy_group (str) – A name for a group of columns to assign to a strategy.

inplace (bool) – Permanent or not. Default is false, because of some testing required sometimes.

suffix (str) – A string to decorate resulting Pandas series name.

color (str | int) – A color from plotly list of colors or its index in that list.

- Return pd.Series:

A serie with tags as values. 1 and -1 for both crosses.

import binpan sym = binpan.Symbol(symbol='ethbusd', tick_interval='1m', limit=300, time_zone='Europe/Madrid') sym.ema(window=10, color='darkgrey') sym.cross(slow='Close', fast='EMA_10') sym.plot(actions_col='Cross_EMA_10_Close', priced_actions_col='EMA_10', labels=['over', 'below'], markers=['arrow-bar-left', 'arrow-bar-right'], marker_colors=['orange', 'blue'])

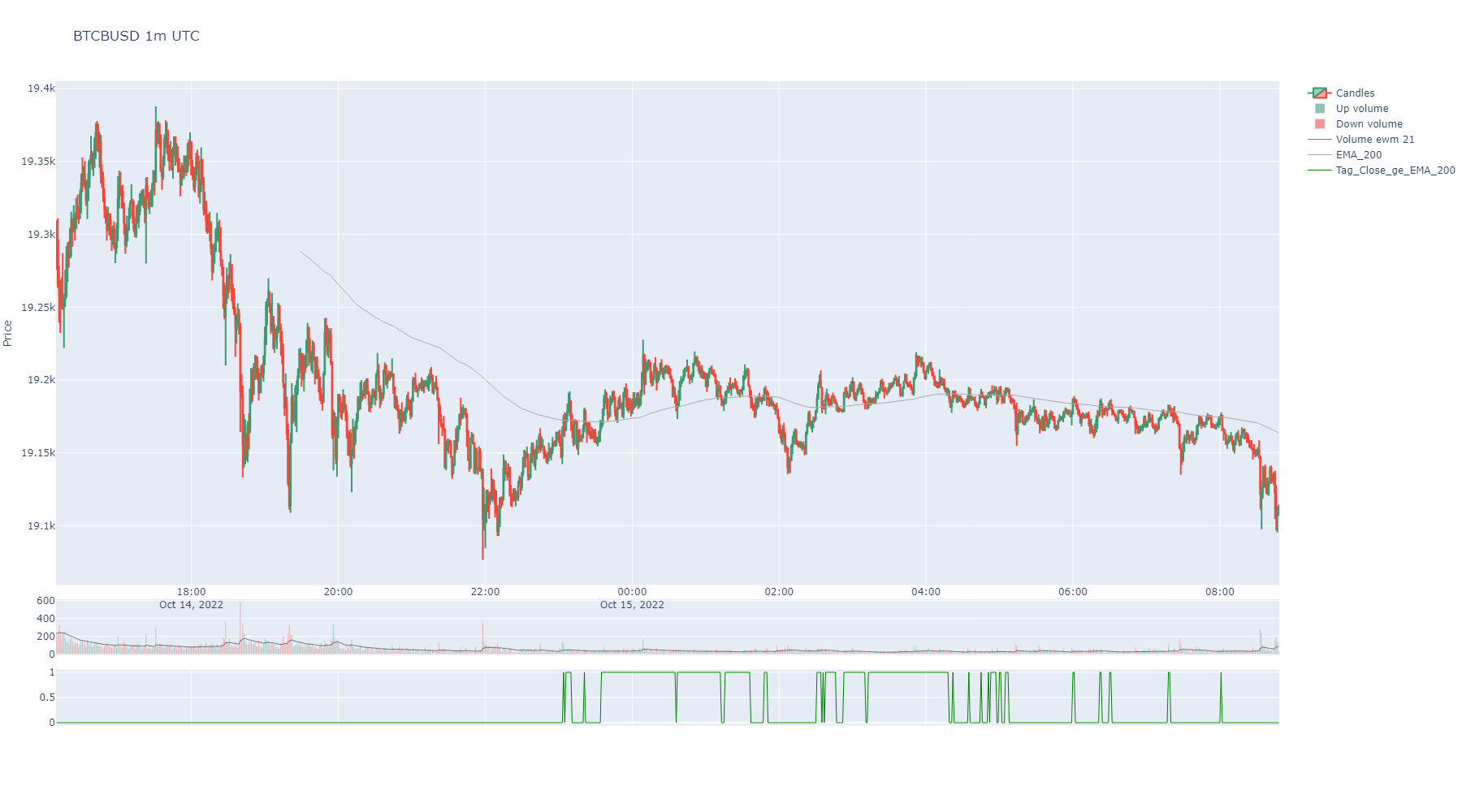

- ema(window: int = 21, column: str = 'Close', inplace=True, suffix: str = '', color: str | int = None, **kwargs) Series¶

Generate technical indicator Exponential Moving Average.

- Parameters:

window (int) – Rolling window including the current candles when calculating the indicator.

column (str) – Column applied. Default is Close.

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

color (str or int) – Color to show when charts. It can be any color from plotly library or index number in that list. <https://community.plotly.com/t/plotly-colours-list/11730>

kwargs – Optional plotly args from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/overlap/ema.py

- Returns:

pd.Series

- eom(length: int = 14, divisor: int = 100000000, drift: int = 1, inplace: bool = True, suffix: str = '', color: str | int = None, **kwargs) Series¶

Ease of Movement (EMV) can be used to confirm a bullish or a bearish trend. A sustained positive Ease of Movement together with a rising market confirms a bullish trend, while a negative Ease of Movement values with falling prices confirms a bearish trend. Apart from using as a standalone indicator, Ease of Movement (EMV) is also used with other indicators in chart analysis.

- Parameters:

length (str) – The short period. Default: 14

divisor (str) – Scaling Constant. Default is 100000000.

drift (str) – The diff period. Default is 1

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

color (str or int) – Is the color to show when plotting or index in that list.

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/volume/eom.py

- Returns:

A Pandas Series

- ffill_window(column: str | int | Series, window: int = 1, inplace=True, replace=False, suffix: str = '', color: str | int = 'blue')¶

It forward fills a value through nans a window ahead.

- Parameters:

window (int) – Times values are shifted ahead. Default is 1.

replace (bool) – Permanent replace for a column with results.

inplace (bool) – Permanent or not. Default is false, because of some testing required sometimes.

suffix (str) – A string to decorate resulting Pandas series name.

color (str | int) – A color from plotly list of colors or its index in that list.

- Return pd.Series:

A series with index adjusted to the new shifted positions of values.

- fractal(period: int = 5, inplace: bool = True, overlap_plot=True, suffix: str = '', colors: list = None) DataFrame¶

The fractal indicator is based on a simple price pattern that is frequently seen in financial markets. Outside of trading, a fractal is a recurring geometric pattern that is repeated on all time frames. From this concept, the fractal indicator was devised. The indicator isolates potential turning points on a price chart. It then draws arrows to indicate the existence of a pattern.

https://www.investopedia.com/terms/f/fractal.asp

- Parameters:

period (int) – Default is 2. Count of neighbour candles to match max or min tags.

inplace (bool) – Make it permanent in the instance or not.

overlap_plot (bool) – If True, it will overlap the indicator plot with the price plot.

suffix (str) – A decorative suffix for the name of the column created.

colors (list) – A list of colors for the indicator dataframe columns. Is the color to show when charts. It can be any color from plotly library or a number in the list of those. Default colors defined. https://community.plotly.com/t/plotly-colours-list/11730

- Return pd.Series:

A serie with 1 or -1 for local max or local min to tag.

- get_maker_taker_buy_ratios(window: int = 14, inplace=True, colors: list = None, suffix: str = '', nans_to_zeros=True) DataFrame¶

Generates the makers versus makers+takers volume ratio by each_kline. Also adds a moving average of the ratio.

- Parameters:

window (int) – The window of the moving average.

inplace (bool) – Permanent or not. Default is false, because of some testing required sometimes.

suffix (str) – A string to decorate resulting Pandas series name.

colors (str or int) – A colors list. Default is [“orange”, “skyblue”].

nans_to_zeros (bool) – If True, NaNs are converted to zeros.

- Returns:

A pandas series with the ratio and the moving average.

- get_market_profile(bins: int = 100, hours: int = None, minutes: int = None, startTime: int | str = None, endTime: int | str = None, from_agg_trades=False, from_atomic_trades=False, time_zone: str = None) DataFrame | None¶

Generates a market profile dataframe from trade or kline data. The market profile is a histogram of trading volumes at different price levels.

- Parameters:

bins – The number of price levels (bins) to include in the market profile.

hours – If specified, only the last ‘hours’ hours of data are used to generate the market profile.

minutes – If specified, only the last ‘minutes’ minutes of data are used to generate the market profile.

startTime – If specified, only data after this timestamp or date (in format %Y-%m-%d %H:%M:%S) are used.

endTime – If specified, only data before this timestamp or date (in format %Y-%m-%d %H:%M:%S) are used.

from_agg_trades – If True, aggregated trades data are used to generate the market profile.

from_atomic_trades – If True, atomic trades data are used to generate the market profile.

time_zone – The time zone to use for time index conversion (e.g., “Europe/Madrid”).

- Returns:

A DataFrame representing the market profile, or None if no suitable data are available.

- get_strategy_columns() list¶

Returns column names starting with “Strategy”.

- Return dict:

Updated strategy groups of columns.

- get_taker_maker_ratio_profile(bins: int = 100, hours: int = None, minutes: int = None, startTime: int | str = None, endTime: int | str = None, from_agg_trades=False, from_atomic_trades=False, time_zone: str = None) DataFrame | None¶

Generates a market profile of the makers versus makers+takers volume ratio by each_kline.

- Parameters:

bins – The number of price levels (bins) to include in the market profile.

hours – If specified, only the last ‘hours’ hours of data are used to generate the market profile.

minutes – If specified, only the last ‘minutes’ minutes of data are used to generate the market profile.

startTime – If specified, only data after this timestamp or date (in format %Y-%m-%d %H:%M:%S) are used.

endTime – If specified, only data before this timestamp or date (in format %Y-%m-%d %H:%M:%S) are used.

from_agg_trades – If True, aggregated trades data are used to generate the market profile.

from_atomic_trades – If True, atomic trades data are used to generate the market profile.

time_zone – The time zone to use for time index conversion (e.g., “Europe/Madrid”).

- Returns:

A DataFrame representing the market profile, or None if no suitable data are available.

- ichimoku(tenkan: int = 9, kijun: int = 26, chikou_span: int = 26, senkou_cloud_base: int = 52, inplace: bool = True, suffix: str = '', colors: list = None) DataFrame¶

The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. It does this by taking multiple averages and plotting them on a chart. It also uses these figures to compute a “cloud” that attempts to forecast where the price may find support or resistance in the future.

- Parameters:

tenkan (int) – The short period. It’s the half sum of max and min price in the window. Default: 9

kijun (int) – The long period. It’s the half sum of max and min price in the window. Default: 26

chikou_span (int) – Close of the next 26 bars. Util for spotting what happened with other ichimoku lines and what happened before Default: 26.

senkou_cloud_base – Period to obtain kumo cloud base line. Default is 52.

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

colors (list) – A list of colors for the indicator dataframe columns. Is the color to show when charts. It can be any color from plotly library or a number in the list of those. Default colors defined. https://community.plotly.com/t/plotly-colours-list/11730

- Returns:

pd.Series

- ma(ma_name: str = 'ema', column_source: str = 'Close', inplace: bool = False, suffix: str = None, color: str | int = None, **kwargs) Series¶

Generic moving average method. Calls pandas_ta ‘ma’ method.

https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/overlap/ma.py

- Parameters:

ma_name (str) – A moving average supported by the generic pandas_ta “ma” function.

column_source (str) – Name of column with data to be used.

inplace (bool) – Permanent or not. Default is false, because of some testing required sometimes.

suffix (str) – A string to decorate resulting Pandas series name.

color (str or int) – A color from plotly list of colors or its index in that list.

kwargs – From https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/overlap/ma.py

- Returns:

pd.Series

- macd(fast: int = 12, slow: int = 26, smooth: int = 9, inplace: bool = True, suffix: str = '', colors: list = None, **kwargs) DataFrame¶

Generate technical indicator Moving Average, Convergence/Divergence (MACD).

- Parameters:

fast (int) – Fast rolling window including the current candles when calculating the indicator.

slow (int) – Slow rolling window including the current candles when calculating the indicator.

smooth (int) – Factor to apply a smooth in values. A smooth is a kind of moving average in short period like 3 or 9.

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

colors (list) –

A list of colors for the MACD dataframe columns. Is the color to show when charts. It can be any color from plotly library or a number in the list of those. Default colors defined.

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/momentum/macd.py

- Returns:

pd.Series

- merge_columns(main_column: str | int | Series, other_column: str | int | Series, sign_other: dict = None, strategy_group: str = '', inplace=True, suffix: str = '', color: str | int = 'grey') Series¶

Predominant serie will be filled nans with values, if existing, from the other serie.

Same kind of index needed.

- Parameters:

main_column (pd.Series) – A serie with nans to fill from other serie.

other_column (pd.Series) – A serie to pick values for the nans.

sign_other (dict) – Replace values by a dict for the “other column”. Default is: {1: -1}

strategy_group (str) – A name for a group of columns to assign to a strategy.

inplace (bool) – Permanent or not. Default is false, because of some testing required sometimes.

suffix (str) – A string to decorate resulting Pandas series name.

color (str | int) – A color from plotly list of colors or its index in that list.

- Return pd.Series:

A merged serie.

- on_balance_volume(inplace: bool = True, suffix: str = '', color: str | int = None, **kwargs) Series¶

On balance indicator.

- Parameters:

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/volume/obv.py

- Returns:

A Pandas Series

- static pandas_ta_indicator(name: str, **kwargs) None¶

Calls any indicator in pandas_ta library with function name as first argument and any kwargs the function will use.

Generic calls are not added to object, just returned.

More info: https://github.com/twopirllc/pandas-ta

- Parameters:

name (str) – A function name. In example: ‘massi’ for Mass Index or ‘rsi’ for RSI indicator.

kwargs – Arguments for the requested indicator. Review pandas_ta info: https://github.com/twopirllc/pandas-ta#features

- Returns:

Whatever returns pandas_ta

Example:

sym = binpan.Symbol(symbol='LUNCBUSD', tick_interval='1m') sym.pandas_ta_indicator(name='ichimoku', **{ 'high': sym.df['High'], 'low': sym.df['Low'], 'close': sym.df['Close'], 'tenkan': 9, 'kijun ': 26, 'senkou ': 52}) ( ISA_9 ISB_26 ITS_9 IKS_26 ICS_26 LUNCBUSD 1m UTC 2022-10-06 23:27:00+00:00 NaN NaN NaN NaN 0.000285 2022-10-06 23:28:00+00:00 NaN NaN NaN NaN 0.000285 2022-10-06 23:29:00+00:00 NaN NaN NaN NaN 0.000285 2022-10-06 23:30:00+00:00 NaN NaN NaN NaN 0.000285 2022-10-06 23:31:00+00:00 NaN NaN NaN NaN 0.000285 ... ... ... ... ... ... 2022-10-07 16:01:00+00:00 0.000292 0.000293 0.000291 0.000291 NaN 2022-10-07 16:02:00+00:00 0.000292 0.000293 0.000292 0.000291 NaN 2022-10-07 16:03:00+00:00 0.000292 0.000293 0.000292 0.000291 NaN 2022-10-07 16:04:00+00:00 0.000292 0.000293 0.000292 0.000291 NaN 2022-10-07 16:05:00+00:00 0.000292 0.000293 0.000292 0.000291 NaN [999 rows x 5 columns], ISA_9 ISB_26 2022-10-10 16:05:00+00:00 0.000292 0.000293 2022-10-11 16:05:00+00:00 0.000292 0.000293 2022-10-12 16:05:00+00:00 0.000292 0.000293 2022-10-13 16:05:00+00:00 0.000292 0.000293 2022-10-14 16:05:00+00:00 0.000292 0.000293 ... ... ... 2022-11-08 16:05:00+00:00 0.000291 0.000292 2022-11-09 16:05:00+00:00 0.000291 0.000292 2022-11-10 16:05:00+00:00 0.000292 0.000292 2022-11-11 16:05:00+00:00 0.000292 0.000292 2022-11-14 16:05:00+00:00 0.000292 0.000292 [26 rows x 2 columns])

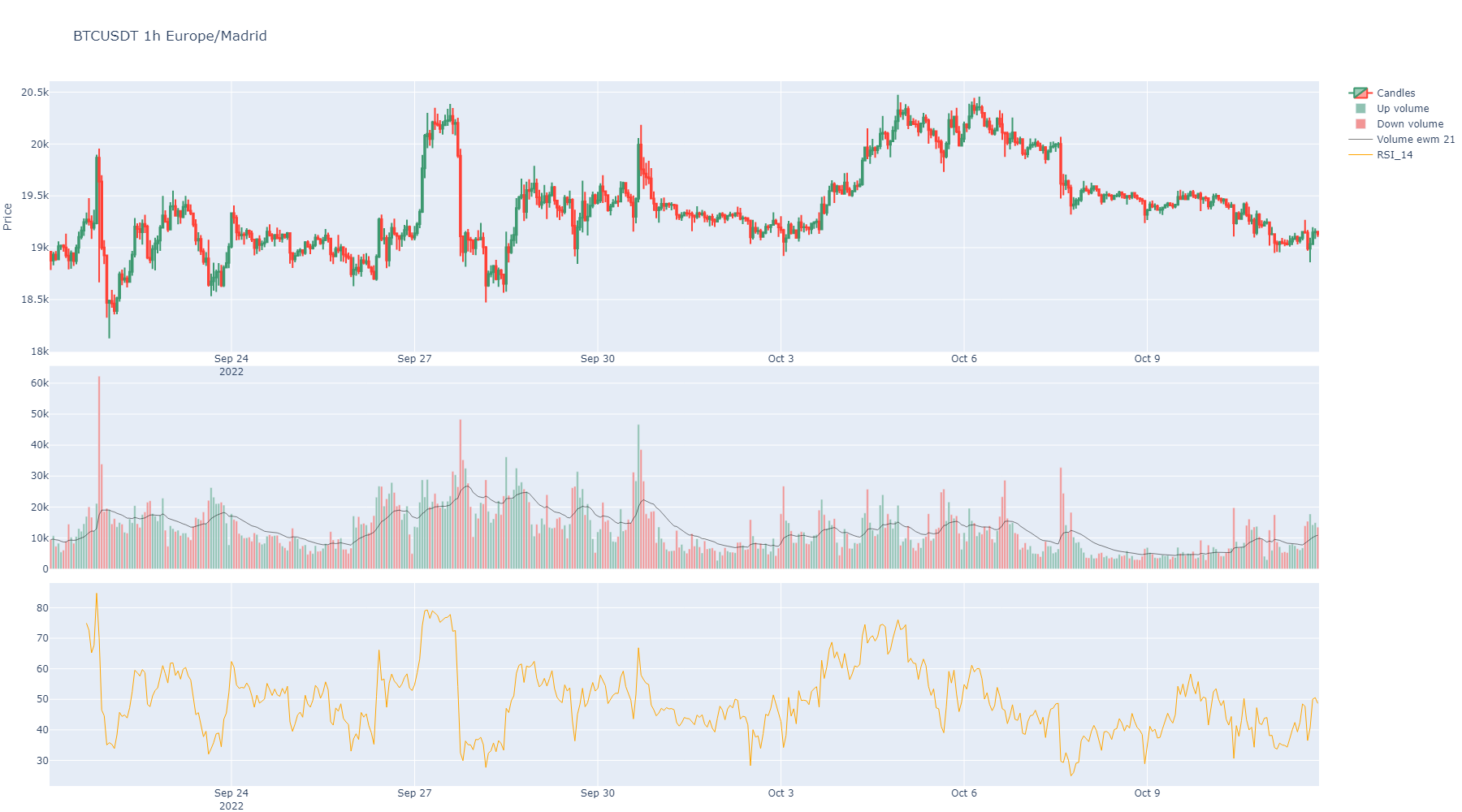

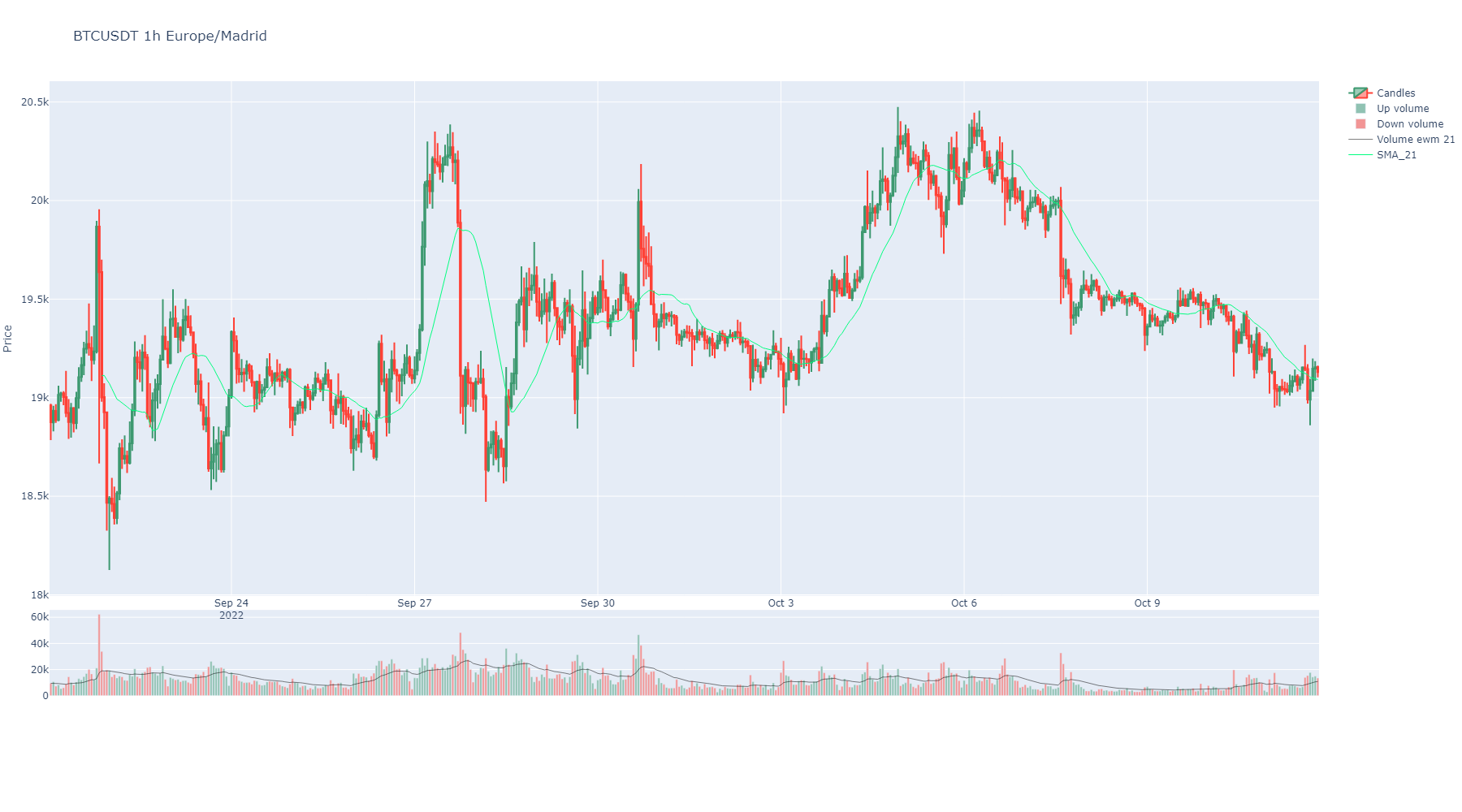

- plot(width: int = 1800, height: int = 1000, candles_ta_height_ratio: float = 0.75, volume: bool = True, title: str = None, yaxis_title: str = 'Price', overlapped_indicators: list = None, priced_actions_col: str = 'Close', actions_col: str = None, marker_labels: dict = None, markers: list = None, marker_colors: list = None, priced_markers: list = None, background_color=None, zoom_start_idx=None, zoom_end_idx=None, support_lines: list = None, support_lines_color: str = 'darkblue', resistance_lines: list = None, resistance_lines_color: str = 'darkred', date: str = None, date_radio: int = 20, show: bool = True, image_path: str = None) str | None¶

Plots a candles figure for the object.

Also plots any other technical indicator grabbed.

- Parameters:

width (int) – Width of the plot.

height (int) – Height of the plot.

candles_ta_height_ratio (float) – Proportion between candles and the other indicators. Not considering overlap ones in the candles plot.

volume (bool) – Plots volume.

title (str) – A tittle for the plot.

yaxis_title (str) – A title for the y axis.

overlapped_indicators (list) – Can declare as overlap in the candles plot some column.

priced_actions_col (str) – Priced actions to plot annotations over the candles, like buy, sell, etc. Under developing.

actions_col (str) – A column containing actions like buy or sell. Under developing.

marker_labels (dict) – Names for the annotations instead of the price. For ‘buy’ tags and ‘sell’ tags. Default is {‘buy’: 1, ‘sell’: -1}

markers (list) – Plotly marker type. Usually, if referenced by number will be a not filled mark and using string name will be a color filled one. Check plotly info: https://plotly.com/python/marker-style/

marker_colors (list) – Colors of the annotations.

priced_markers (list) – Explicit operation markers to overlay on exact points: a list of dicts

{'time', 'price', 'side', 'label'?}.side‘buy’ draws a green ▲ (label below), otherwise a red ▼ (label above).timeis a positional candle index (int) or a timestamp (snapped to the nearest candle);priceis the exact y level. Compatible with support/resistance lines and action columns (they overlay together).background_color (str) – Sets background color. Select a valid plotly color name.

zoom_start_idx (int) – It can zoom to an index interval.

zoom_end_idx (int) – It can zoom to an index interval.

support_lines (list) – A list of prices to plot horizontal lines in the candles plot for supports or any other level.

support_lines_color (str) – A color for horizontal lines, ‘darkblue’ is by default.

resistance_lines (list) – A list of prices to plot horizontal lines in the candles plot for resistances or any other level.

resistance_lines_color (str) – A color for horizontal lines, ‘darkred’ is by default.

date (str) – A date in string format to plot a zoom of a radio of klines up and down in time. Useful to inspect dates. Incompatible with zoom_start_idx and zoom_end_idx. Strings formatted as “2022-05-11 06:45:42”

date_radio (str) – A radio in klines to plot a zoom around a date.

- plot_agg_trades_size(max_size: int = 60, height: int = 1000, logarithmic: bool = False, overlap_prices: bool = True, group_big_data: int = None, shifted: int = 1, title: str = None, size_column: str = 'Quantity', width: int = None, horizontal_lines: list = None, show: bool = True, image_path: str = None) str | None¶

It plots a time series graph plotting aggregated trades sized by quantity and color if taker or maker buyer.

- Parameters:

max_size (int) – Max size for the markers. Default is 60. Useful to show whales operating.

height (int) – Default is 1000.

logarithmic (bool) – If logarithmic, then “y” axis scale is shown in logarithmic scale.

group_big_data (int) – Deprecated, ignored. Kept for backward compatibility.

shifted (bool) – If True, shifts prices to plot klines one step to the right, that’s more natural to see trades action in price.

overlap_prices (bool) – If True, plots overlap line with High and Low prices.

title – Graph title.

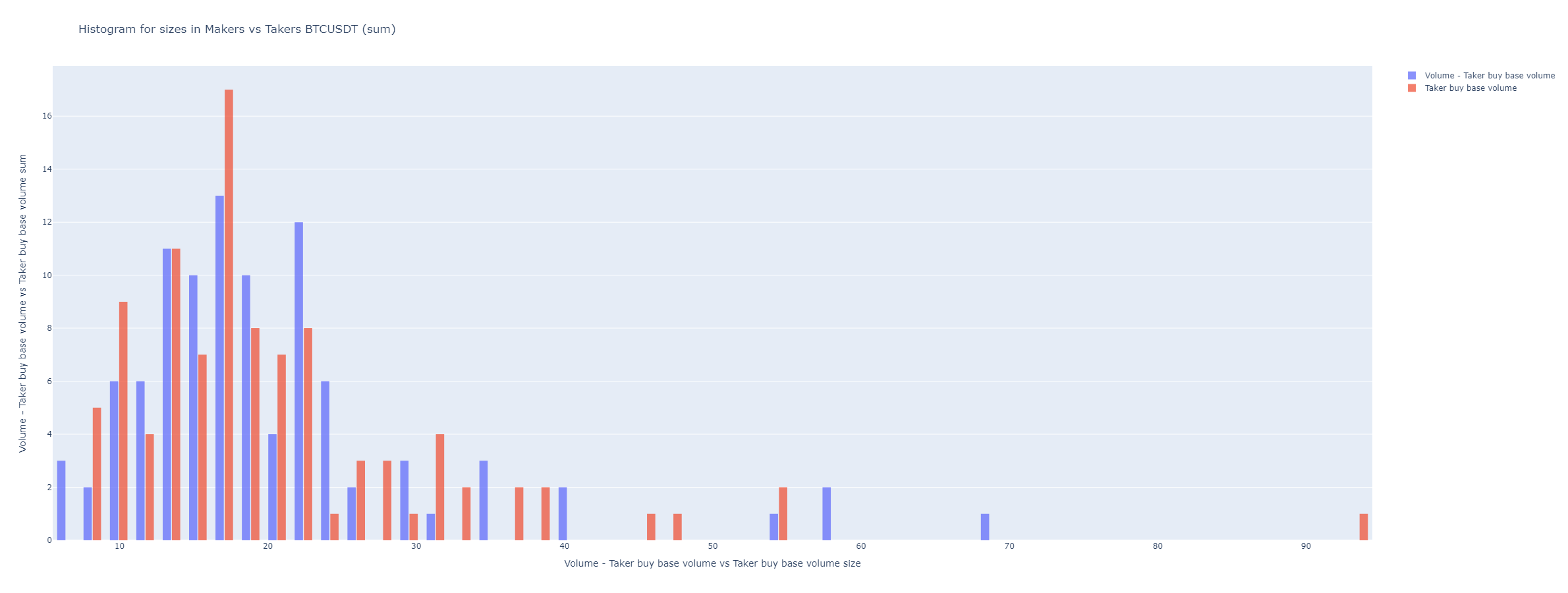

- plot_aggression_sizes(bins=50, hist_funct='sum', height=900, from_trades=False, title: str = None, total_volume_column: str = None, partial_vol_column: str = None, **kwargs_update_layout) str | None¶

Binance fees can be cheaper for maker orders, many times when big traders, like whales, are operating . Showing what are doing makers.

It shows which kind of volume or trades came from, aggressive_sellers or aggressive_byers.

Can be useful finding support and resistance zones.

- Parameters:

bins – How many bars.

hist_funct – The way graph data is showed. It can be ‘mean’, ‘sum’, ‘percent’, ‘probability’, ‘density’, or ‘probability density’

height – Height of the graph.

from_trades – Requieres grabbing trades before.

title – A title.

total_volume_column – The column with the total volume. It defaults automatically.

partial_vol_column – The column with the partial volume. It defaults automatically. API shows maker or taker separated volumes.

kwargs_update_layout – Optional

- plot_atomic_trades_size(max_size: int = 60, height: int = 1000, logarithmic: bool = False, overlap_prices: bool = True, group_big_data: int = None, shifted: int = 1, title: str = None, size_column: str = 'Quantity', width: int = None, horizontal_lines: list = None, show: bool = True, image_path: str = None) str | None¶

It plots a time series graph plotting atomic trades sized by quantity and color if taker or maker buyer.

- Parameters:

max_size (int) – Max size for the markers. Default is 60. Useful to show whales operating.

height (int) – Default is 1000.

logarithmic (bool) – If logarithmic, then “y” axis scale is shown in logarithmic scale.

group_big_data (int) – Deprecated, ignored. Kept for backward compatibility.

shifted (bool) – If True, shifts prices to plot klines one step to the right, that’s more natural to see trades action in price.

overlap_prices (bool) – If True, plots overlap line with High and Low prices.

title – Graph title.

- plot_market_profile(bins: int = 100, hours: int = None, minutes: int = None, startTime: int | str = None, endTime: int | str = None, height=900, from_agg_trades=False, from_atomic_trades=False, title: str = None, time_zone: str = None, **kwargs_update_layout) str | None¶

Plots volume histogram by prices segregated aggressive buyers from sellers.

- Parameters:

bins (int) – How many bars.

hours (int) – If passed, it use just last passed hours for the plot.

minutes (int) – If passed, it use just last passed minutes for the plot.

startTime (int | str) – If passed, it use just from the timestamp or date in format (%Y-%m-%d %H:%M:%S: 2022-05-11 06:45:42)) for the plot.

endTime (int | str) – If passed, it use just until the timestamp or date in format (%Y-%m-%d %H:%M:%S: 2022-05-11 06:45:42)) for the plot.

height – Height of the graph.

from_agg_trades – Requieres grabbing aggregated trades before.

from_atomic_trades – Requieres grabbing atomic trades before.

title – A title.

time_zone (str) – A time zone for time index conversion. Example: “Europe/Madrid”

kwargs_update_layout – Optional

- plot_orderbook(accumulated=True, title='Depth orderbook plot', height=800, plot_y='Quantity', **kwargs) str | None¶

Plots orderbook depth.

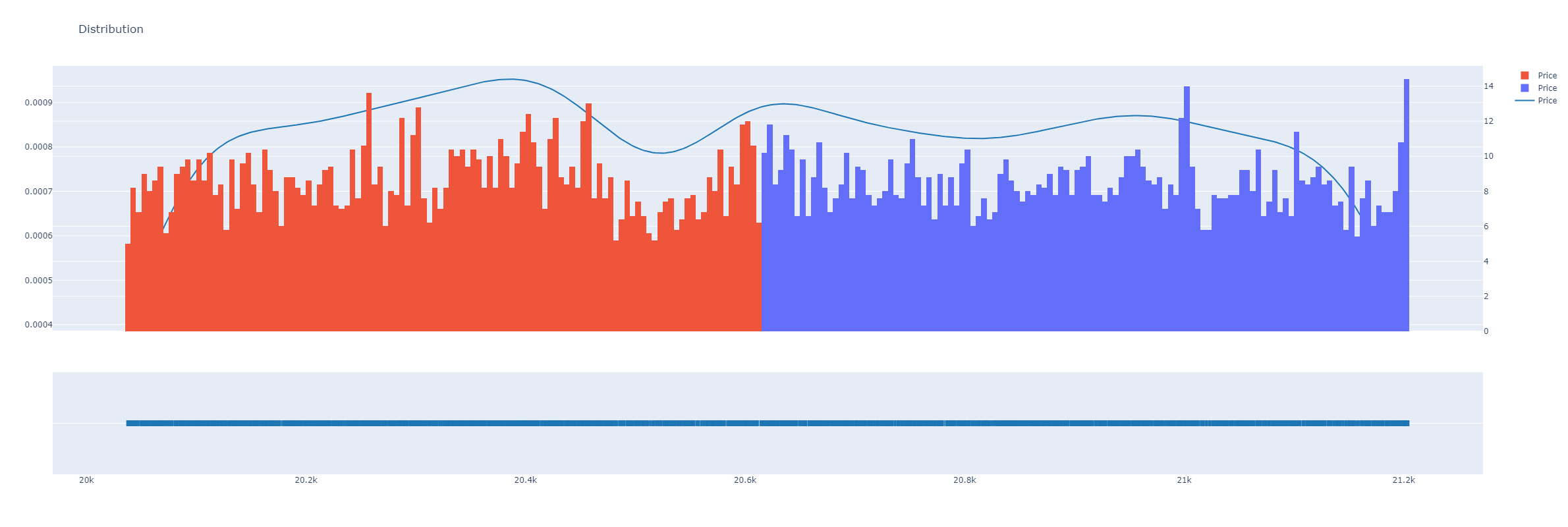

- plot_orderbook_density(x_col='Price', color='Side', bins=300, histnorm: str = 'density', height: int = 800, title: str = None, **update_layout_kwargs) str | None¶

Plot a distribution plot for a dataframe column. Plots line for kernel distribution.

- Parameters:

x_col (str) – Column name for x-axis data.

color (str) – Column name with tags or any values for using as color scale.

bins (int) – Columns in histogram.

histnorm (str) – One of ‘percent’, ‘probability’, ‘density’, or ‘probability density’ from plotly express documentation. https://plotly.github.io/plotly.py-docs/generated/plotly.express.histogram.html

height (int) – Plot sizing.

title (str) – A title string

- plot_reversal(min_height: int = None, min_reversal: int = None, text_index: bool = True, from_atomic: bool = False, **kwargs) str | None¶

Plots reversal candles. It requires aggregated or atomic trades fetched previously.

BinPan manages aggregated trades from binance API.

- Parameters:

- Returns:

Example:

import binpan ltc = binpan.Symbol(symbol='ltcbtc', tick_interval='5m', time_zone = 'Europe/Madrid', time_index = True, closed = True, hours=5) ltc.get_trades() ltc.get_reversal_candles() ltc.plot_reversal()

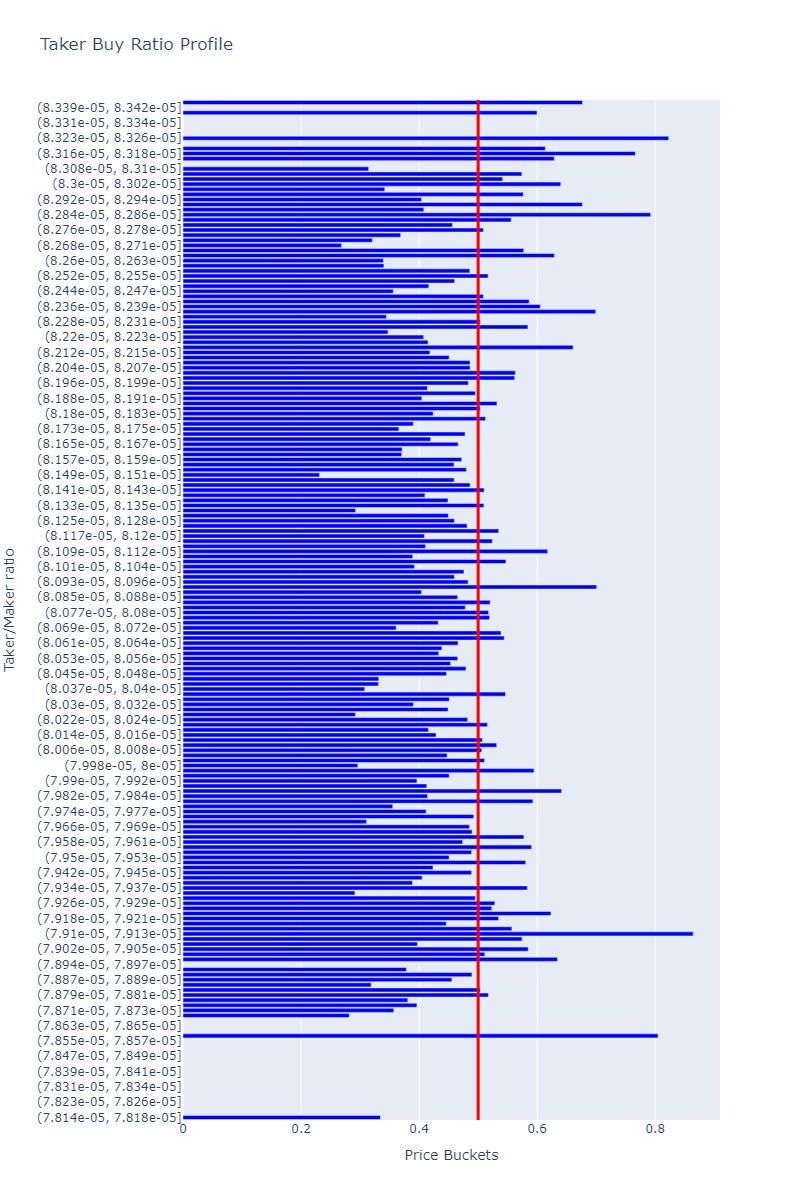

- plot_taker_maker_ratio_profile(bins: int = 100, hours: int = None, minutes: int = None, startTime: int | str = None, endTime: int | str = None, from_agg_trades=False, from_atomic_trades=False, time_zone: str = None, title: str = 'Taker Buy Ratio Profile', height=1200, width=800, **kwargs_update_layout) str¶

Plots taker vs maker ratio profile.

- Parameters:

bins (int) – How many bars.

hours (int) – If passed, it use just last passed hours for the plot.

minutes (int) – If passed, it use just last passed minutes for the plot.

startTime (int | str) – If passed, it use just from the timestamp or date in format (%Y-%m-%d %H:%M:%S: 2022-05-11 06:45:42)) for the plot.

endTime (int | str) – If passed, it use just until the timestamp or date in format (%Y-%m-%d %H:%M:%S: 2022-05-11 06:45:42)) for the plot.

height – Height of the graph.

width – Width of the graph.

from_agg_trades – Requieres grabbing aggregated trades before.

from_atomic_trades – Requieres grabbing atomic trades before.

title – A title.

time_zone (str) – A time zone for time index conversion. Example: “Europe/Madrid”

kwargs_update_layout – Optional

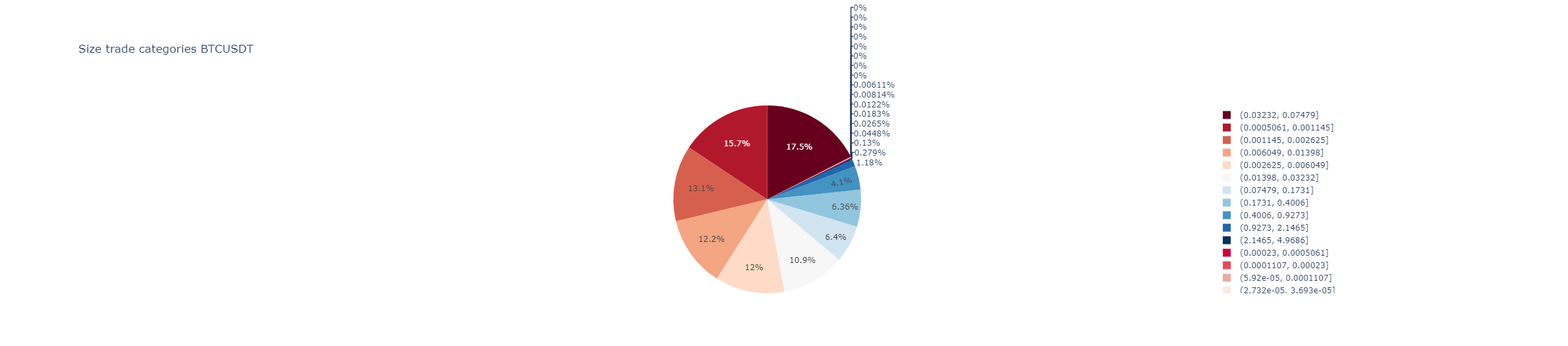

- plot_trades_pie(categories: int = 25, logarithmic=True, title: str = None) str | None¶

Plots a pie chart. Useful profiling size of trades. Size can be distributed in a logarithmic scale.

- Parameters:

categories – How many groups of sizes.

logarithmic – Logarithmic scale to show more small sizes.

title – A title for the plot.

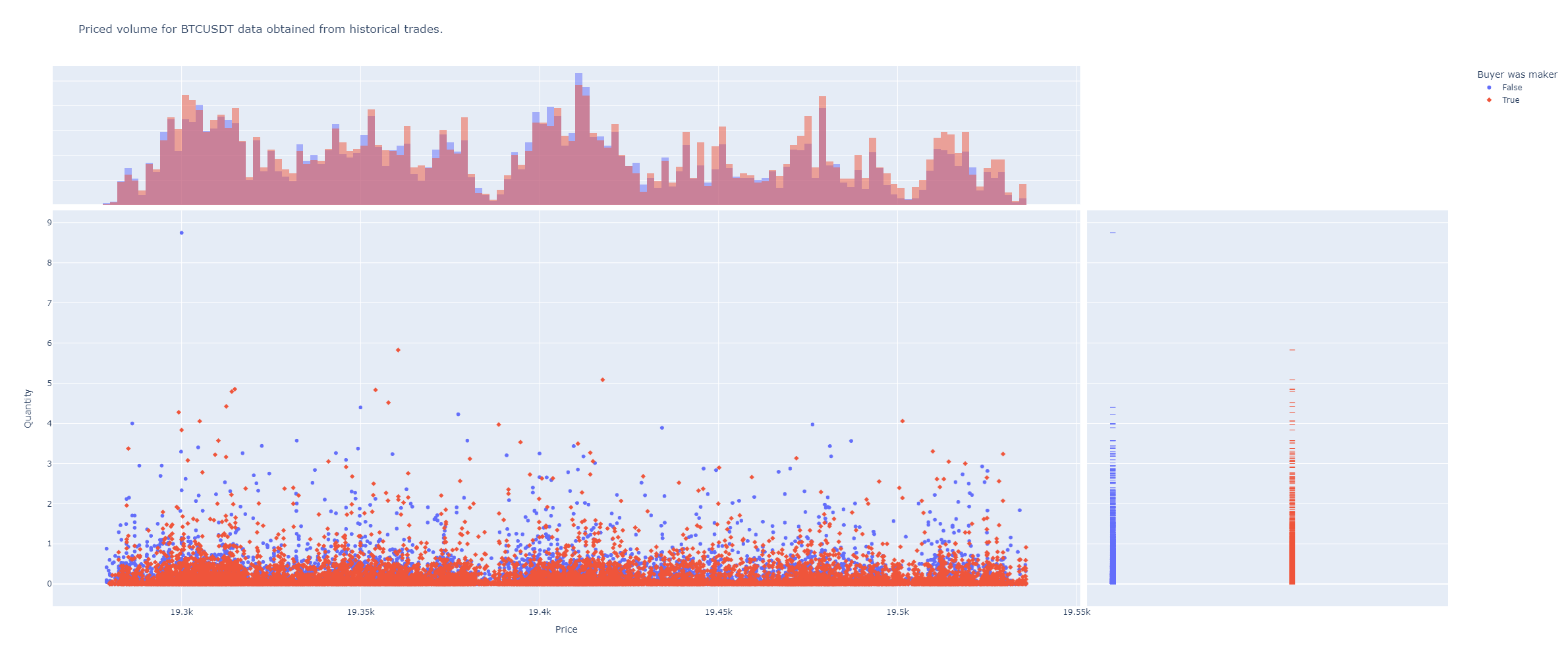

- plot_trades_scatter(x: str = None, y: str = None, dot_symbol='Buyer was maker', color: str = None, marginal=True, from_trades=True, height=1000, color_referenced_to_y=True, **kwargs) str | None¶

A scatter plot showing each price level volume or trades.

It can be useful finding support and resistance zones.

- Parameters:

dot_symbol – Column with discrete values to assign different symbols for the plot marks.

x – Name of the column with prices. From trades or candles.

y – Name of the column with sizes. From trades or candles.

color – Column with values to use in color scale.

marginal – Show or not lateral plots.

from_trades – Uses trades instead of candles. Useful to avoid grabbing very long time intervals. Result should be similar.

height – Height of the plot.

color_referenced_to_y – Scales color in y axis.

kwargs – Optional plotly args.

- plot_volume_profile(bins: int = 50, value_area_pct: float = 0.7, from_agg_trades: bool = False, from_atomic_trades: bool = False, hours: int = None, minutes: int = None, startTime: int | str = None, endTime: int | str = None, time_zone: str = None, title: str = None, height: int = 900, width: int = None, horizontal_lines: list = None, priced_markers: list = None, show: bool = True, image_path: str = None) str | None¶

Volume Profile (VPVR): velas + histograma horizontal de volumen, con POC y Value Area.

Dibuja las velas a la izquierda y, compartiendo el eje de precio, un histograma horizontal del volumen por nivel a la derecha. Resalta la Value Area, traza el POC y marca los LVN (huecos por donde el precio viaja rapido). Util para ver imanes y soportes/resistencias por aceptacion. Los numeros (POC/VAH/VAL/HVN/LVN) se obtienen con

volume_profile().- Parameters:

bins (int) – numero de niveles del histograma. Default 50.

value_area_pct (float) – fraccion del volumen dentro de la Value Area. Default 0.70.

from_agg_trades (bool) – perfil fino desde aggregated trades (requiere

get_agg_trades()antes).from_atomic_trades (bool) – perfil desde atomic trades (requiere

get_atomic_trades()antes).hours (int) – si se pasa, solo las ultimas ‘hours’ horas.

minutes (int) – si se pasa, solo los ultimos ‘minutes’ minutos.

startTime – timestamp/fecha de inicio (rango fijo).

endTime – timestamp/fecha de fin (rango fijo).

time_zone (str) – zona horaria para el indice temporal.

title (str) – titulo del grafico.

height (int) – alto px. Default 900.

width (int) – ancho px. Si None, autosize.

horizontal_lines (list) – precios extra (entrada/stop/TP) como lineas discontinuas.

priced_markers (list) – marcadores de operacion (▲ compra / ▼ venta) en puntos exactos sobre las velas: lista de

{'time', 'price', 'side', 'label'?}(verset_price_markers).show (bool) – si True (default) abre la figura interactiva; False para uso headless/servidor.

image_path (str) – ruta del PNG de salida. Por defecto

last_plot.pngen el cwd.

- Returns:

ruta absoluta de la imagen exportada, o None si falla.

- profit_hour(column: str = None) float¶

It returns win or loos quantity per hour. Just compares first and last value. Expected datetime index. If not column passed, it will search for an Evaluation column.

- Parameters:

column (str) – A column in the BinPan’s DataFrame with values to check profit with expected datetime index.

- Return float:

Resulting return of inversion.

- remove_plot_info_associated_columns(columns: list, row_level: str) list¶

Completely remove plot info for a column in main dataframe of klines.

- remove_plot_info_for_column(column: str) None¶

Remove plot info for a column in main dataframe of klines. :param column:

- roc(length: int = 1, escalar: int = 100, inplace: bool = True, suffix: str = '', color: str | int = None, **kwargs) Series¶

The Rate of Change (ROC) is a technical indicator that measures the percentage change between the most recent price and the price “n” day’s ago. The indicator fluctuates around the zero line.

- Parameters:

length (str) – The short period. Default: 1

escalar (str) – How much to magnify. Default: 100.

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

color (str or int) – Is the color to show when plotting or index in that list.

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/momentum/roc.py

- Returns:

A Pandas Series

- roi(column: str = None) float¶

It returns win or loos percent for a evaluation column. Just compares first and last value increment by the first price in percent. If not column passed, it will search for an Evaluation column.

- Parameters:

column (str) – A column in the BinPan’s DataFrame with values to check ROI (return of inversion).

- Return float:

Resulting return of inversion.

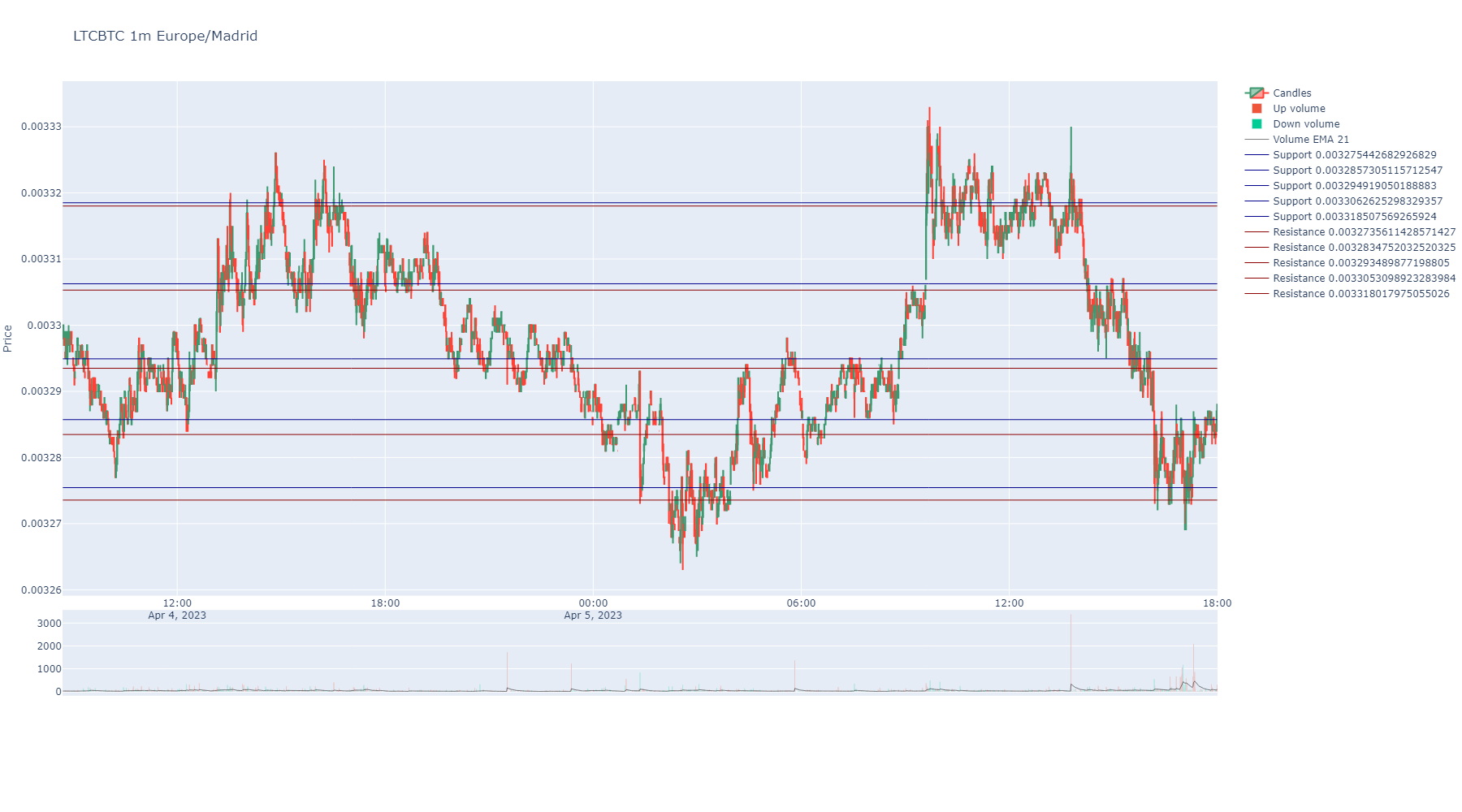

- rolling_support_resistance(minutes_window: int = None, time_steps_minutes: int = None, discrete_interval: str = None, from_atomic: bool = False, from_aggregated: bool = False, max_clusters: int = 5, by_quantity: bool = True, simple: bool = True, inplace: bool = True, delayed: int = 0, colors: list = None) DataFrame | None¶

Calculate support and resistance levels for the Symbol based on either atomic trades or aggregated trades in a rolling window. Also from klines supported, but less accurate. It returns a pandas dataframe with each column representing ordered levels from lower to higher for support and resistance. The function iterates in steps of a minutes quantity or a discrete interval.

If discrete_interval is passed, it will ignore time_steps_minutes and minutes_window and will use this interval to calculate the rolling support and resistance minutes_window and time_steps_minutes. It can be any of the binance kline ones: ‘1m’, ‘3m’, ‘5m’, ‘15m’, ‘30m’, ‘1h’, ‘2h’, ‘4h’, etc

The parameter delayed is useful when you want to calculate the rolling support and resistance with a delay. For example, if you want to calculate the rolling support and resistance with the last 5 minutes of data, but you want to project it 5 minutes after the last minute of the window, you can pass delayed=1 (1 step of the interval selected). Useful for projecting support and resistance levels in the future.

If simple parameter is True, it will calculate support and resistance levels merged. Just levels. Default is True.

Example: If you want to calculate the rolling support and resistance with and interval of 24h and a delayed of 1, this will add past 24h support and resistance levels to the current dataframe

my_symbol.rolling_support_resistance(discrete_interval='1d', delayed=1)

Example: Not discrete mode but same 24 h intervals and not delayed.

sym.rolling_support_resistance(minutes_window=24*60, time_steps_minutes=24*60, max_clusters=5)

- Parameters:

minutes_window (int) – A rolling window of time in minutes. Whe using trades, it will calculate window by time index.

time_steps_minutes (int) – Loop steps in minutes. Default is 10. Each step will calculate a new window data.

discrete_interval (str) – If passed, it will ignore time_steps_minutes and minutes_window and will use this interval to calculate the rolling support and resistance. It can be any of the following: ‘1m’, ‘3m’, ‘5m’, ‘15m’, ‘30m’, ‘1h’, ‘2h’, ‘4h’, etc

from_atomic (bool) – If True, support and resistance levels will be calculated using atomic trades.

from_aggregated (bool) – If True, support and resistance levels will be calculated using aggregated trades.

max_clusters (int) – If passed, fixes count of levels of support and resistance. Default is 5.

by_quantity (float) – It takes each price into account by how many times the specified quantity appears in “Quantity” column.

simple (bool) – If True, it will calculate support and resistance levels merged. Just levels. Default is True.

inplace (bool) – If True, it will replace the current dataframe with the new one. Default is True.

delayed (int) – If passed, it will project the rolling support and resistance levels in the future. Default is 0 and means 0 windows projected in the future.

colors (list) – A list of colors for the indicator dataframe columns. Is the color to show when charts. It can be any color from plotly library or a number in the list of those. Default colors defined. https://community.plotly.com/t/plotly-colours-list/11730

- Return pd.DataFrame:

A pandas dataframe with each column representing ordered levels from higher to lower for support and resistance.

- rsi(length: int = 14, inplace: bool = True, suffix: str = '', color: str | int = None) Series¶

Relative Strength Index (RSI).

- Parameters:

- Returns:

A Pandas Series

- set_plot_axis_group(indicator_column: str = None, my_axis_group: str = None) dict¶

Internal control formatting plots. Can be used to change plot filling mode for pairs of indicators when.

- Parameters:

indicator_column (str) – column name

my_axis_group – Fill mode for indicator. Color can be forced to fill to zero line with “tozeroy” or between two indicators in same axis group with “tonexty”.

- Return dict:

columns with its assigned fill mode.

- set_plot_color(indicator_column: str = None, color: int | str = None) dict¶

Internal control formatting plots. Can be used to change plot color of an indicator.

- Parameters:

indicator_column (str) – column name

color – reassign color to column name

- Return dict:

columns with its assigned colors when charts.

- set_plot_color_fill(indicator_column: str = None, color_fill: str | bool = None) dict¶

Internal control formatting plots. Can be used to change plot color of an indicator.

- Parameters:

indicator_column (str) – column name

color_fill – Color can be forced to fill to zero line. For transparent colors use rgba string code to define color. Example for transparent green ‘rgba(26,150,65,0.5)’ or transparent red ‘rgba(204,0,0,0.5)’

- Return dict:

columns with its assigned colors when charts.

- set_plot_filled_mode(indicator_column: str = None, fill_mode: str = None) dict¶

Internal control formatting plots. Can be used to change plot filling mode for pairs of indicators when.

- Parameters:

indicator_column (str) – column name

fill_mode – Fill mode for indicator. Color can be forced to fill to zero line with “tozeroy” or between two indicators in same axis group with “tonexty”.

- Return dict:

columns with its assigned fill mode.

- set_plot_row(indicator_column: str = None, row_position: int = None) dict¶

Internal control formatting plots. Can be used to change plot subplot row of an indicator.

- Parameters:

indicator_column (str) – column name

row_position – reassign row_position to column name

- Return dict:

columns with its assigned row_position in subplots when charts.

- set_plot_splitted_serie_couple(indicator_column_up: str = None, indicator_column_down: str = None, splitted_dfs: list = None, color_up: str = 'rgba(35, 152, 33, 0.5)', color_down: str = 'rgba(245, 63, 39, 0.5)') dict¶

Modify the control for splitted series in plots with colored area in two colors by relative position.

If no params passed, then returns dict actual contents.

- Parameters:

indicator_column_up (str) – An existing column from a BinPan Symbol’s class dataframe to plot as up serie (green color).

indicator_column_down (str) – An existing column from a BinPan Symbol’s class dataframe to plot as down serie (red clor).

splitted_dfs (tuple) – A list of pairs of a splitted dataframe by two columns.

color_up – An rgba formatted color: https://rgbacolorpicker.com/

color_down – An rgba formatted color: https://rgbacolorpicker.com/

- Return dict:

A dictionary with auxiliar data about plot areas with two colours by relative position.

- set_plotting_volume_ma(window: int = 21) None¶

Set a window for plotting volume moving average on the candles plot when volumen bars are plotted.

- Parameters:

window (int) – A window for the moving average.

- set_strategy_groups(column: str, group: str, strategy_groups: dict = None) dict¶

Returns strategy_groups for BinPan DataFrame.

- shift(column: str | int | Series, window=1, strategy_group: str = '', inplace=True, suffix: str = '', color: str | int = 'grey') Series¶

It shifts a candle ahead by the window argument value (or backwards if negative)

- Parameters:

window (int) – Number of candles moved ahead.

strategy_group (str) – A name for a group of columns to assign to a strategy.

inplace (bool) – Permanent or not. Default is false, because of some testing required sometimes.

suffix (str) – A string to decorate resulting Pandas series name.

color (str | int) – A color from plotly list of colors or its index in that list.

- Return pd.Series:

A serie with tags as values.

- sma(window: int = 21, column: str = 'Close', inplace=True, suffix: str = '', color: str | int = None, **kwargs) Series¶

Generate technical indicator Simple Moving Average.

- Parameters:

window (int) – Rolling window including the current candles when calculating the indicator.

column (str) – Column applied. Default is Close.

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

color (str or int) – Color to show when charts. It can be any color from plotly library or a number in the list of those. <https://community.plotly.com/t/plotly-colours-list/11730>

kwargs – Optional plotly args from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/overlap/sma.py

- Returns:

pd.Series

- stoch(k_length: int = 14, stoch_d=3, k_smooth: int = 1, inplace: bool = True, suffix: str = '', colors: list = None, **kwargs) DataFrame¶

Stochastic Oscillator with a fast and slow exponential moving averages.

- Parameters:

k_length (int) – The Fast %K period. Default: 14

stoch_d (int) – The Slow %K period. Default: 3

k_smooth (int) – The Slow %D period. Default: 3

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

colors (list) – Is the color to show when charts.

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/momentum/stoch.py

- Returns:

A Pandas DataFrame

- stoch_rsi(rsi_length: int = 14, k_smooth: int = 3, d_smooth: int = 3, inplace: bool = True, suffix: str = '', colors: list = None, **kwargs) DataFrame¶

Stochastic Relative Strength Index (RSI) with a fast and slow exponential moving averages.

- Parameters:

rsi_length (int) – Default is 21

k_smooth (int) – Smooth fast line with a moving average of some periods. default is 3.

d_smooth (int) – Smooth slow line with a moving average of some periods. default is 3.

inplace (bool) – Make it permanent in the instance or not.

suffix (str) – A decorative suffix for the name of the column created.

colors (list) – Is the color to show when charts.

kwargs – Optional from https://github.com/twopirllc/pandas-ta/blob/main/pandas_ta/momentum/stochrsi.py

- Returns:

A Pandas DataFrame

- strategy_from_tags_crosses(columns: list = None, strategy_group: str = '', matching_tag=1, method: str = 'all', tag_reversed_match: bool = False, inplace=True, suffix: str = '', color: str | int = 'magenta', reversed_match=-1) Series¶

Checks where all tags and cross columns get value “1” at the same time. And also gets points where all tags gets value of “0” and cross columns get “-1” value.

- Parameters:

columns (list) – A list of Tag and Cross columns with numeric o 1,0 for tags and 1,-1 for cross points.

strategy_group (str) – A name for a group of columns to restrict application of strategy. If both columns and strategy_group passed, a interjection between the two arguments is applied.

tag_reversed_match (bool) – If enabled, all zeros or minus ones tag and cross columns are interpreted as reversed match, this will enable tagging those.

matching_tag (any) – A tag to search for the strategy where will be revised method for matched rows.

method (str) – Can be ‘all’ or ‘any’. It produces a match when all or any columns are matching tags.

reversed_match (any) – A tag for the all/any not matched strategy rows.

inplace (bool) – Permanent or not. Default is false, because of some testing required sometimes.

suffix (str) – A string to decorate resulting Pandas series name.